The US-Israeli war against Iran has once again propelled gold into the spotlight as global investors seek safe havens amid fears of a prolonged regional conflict. Following the killing of Iran’s Supreme Leader Ayatollah Ali Khamenei, the country has intensified its retaliatory attacks across the Middle East, while US President Trump has warned that the war could last four to five weeks and possibly go “far longer”.

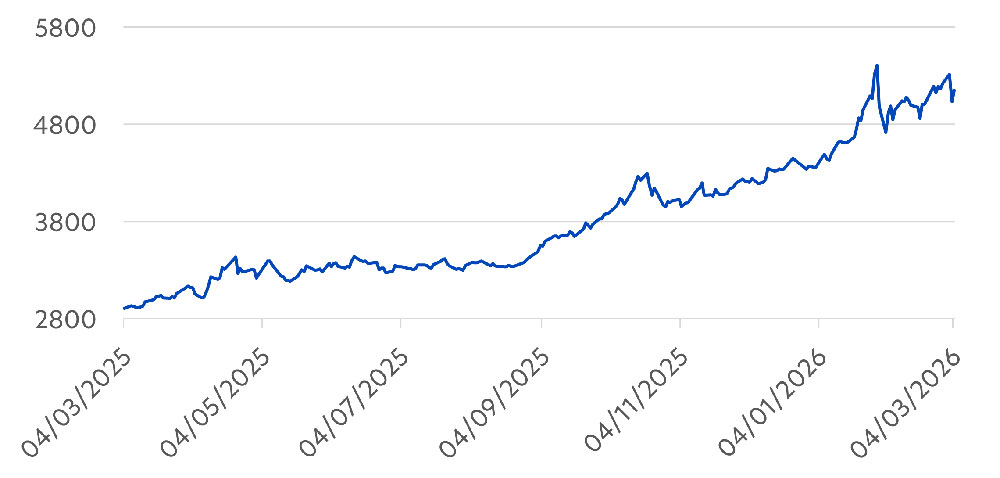

With geopolitical risks showing little sign of easing, safe haven demand is likely to continue underpinning gold prices, even as oil-driven inflation concerns introduce occasional bouts of volatility. Having risen 65 percent in 2025, gold is up around 18 percent in the year to date1.

Fig 1: The rise in gold prices over the past year

Source: UOBAM, Bloomberg, as of 4 March 2026

Gold during geopolitical crises

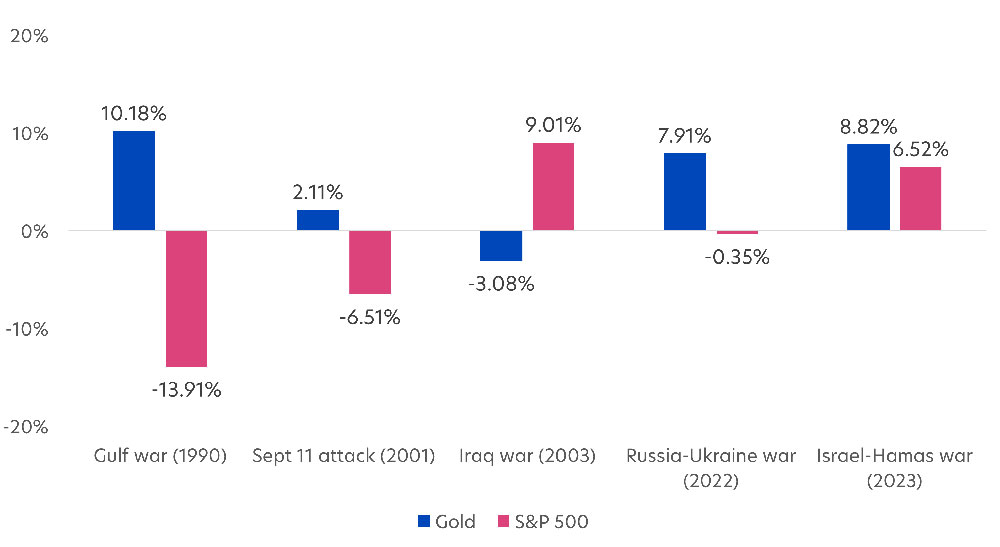

Gold has historically served as a portfolio stabiliser during periods of global stress. It tends to remain resilient in environments marked by elevated geopolitical uncertainty and macro regime change. Across major geopolitical crises over the past three decades, gold and equities have frequently moved in opposite directions, underscoring its long-standing role as a portfolio diversifier2.

Fig 2: Performance of gold and S&P 500 across major geopolitical events

Source: UOBAM, Bloomberg, as of 4 March 2026. Gold prices reflect the LBMA gold price USD. Time frames chosen are two-month analytical windows designed to encompass the lead-up, occurrence, and initial market impact of each geopolitical event.

This behavior is rooted in gold’s low correlation to global equities in most market environments. When stock markets fall, particularly during periods of sharp risk aversion, gold tends to hold its value or even appreciate, providing a partial offset to equity losses within a diversified portfolio.

That said, this may not happen all the time. The Iraq War of 2003 is a notable exception where gold weakened even as equities recovered quickly. The swift and initially successful nature of the invasion reduced the market’s perceived need for safe-haven assets, resulting in a pullback in gold prices.

Ultimately, these dynamics reinforce a simple point: while gold’s reaction to individual crises may vary, it has consistently demonstrated an ability to diversify risk over the long term, cementing its relevance for investors.

Gold continues to be in demand

Beyond today’s geopolitical uncertainties, the underlying structural reasons for considering gold continue to hold true.

1. Strong central bank buying

Central banks, particularly in emerging markets, have continued to steadily increase their gold holdings as they diversify away from US Treasuries amid concerns over rising US debt and fiscal deficits. Notably, 43 percent of global monetary authorities surveyed by the World Gold Council expect to raise their gold reserves over the coming year, signalling that this structural buying trend is set to continue3.

2. A hedge against inflation

The Middle East conflict has fuelled concerns that higher oil prices will ultimately feed through to consumer and producer inflation, raising the risk of renewed price pressures. These conditions could make gold more attractive, given its historical role as a reliable store of value and inflation hedge.

3. Renewed ETF interest

Strong investor interest has driven sizeable inflows into gold ETFs this year. Many investors are seeking safety amid geopolitical tensions, while others are positioning for a weaker US dollar and potential Fed rate cuts. As of end February 2026, US-listed gold ETFs had attracted US$10.5 billion in inflows, a sharp increase from the US$6.3 billion recorded over the same period in 20254. While steady central bank buying provides a solid foundation for the market, ETF flows tend to amplify price moves, adding momentum when investor demand strengthens.

Gold mining stocks: A different way to gain exposure

While the case for gold remains strong, investors seeking exposure to the metal have more than one pathway. Beyond physical gold and ETFs, gold mining equities offer an alternative route. Although they may not exhibit the safe-haven qualities of gold itself, their performance is closely tied to gold prices.

When gold moves higher, miners typically benefit from stronger revenues and wider profit margins, which can translate into share price gains. However, the reverse is also true. When gold prices fall, or when miners face rising costs, operational setbacks, or geopolitical disruptions in key mining regions, their share prices can decline more sharply than the metal itself.

This means gold mining equities carry a higher risk profile, but they also offer a more growth-oriented way to express a positive gold view and can complement the defensive qualities of physical gold or gold-backed ETFs.

Spotlight on the United Gold & General Fund

For investors seeking a diversified, professionally managed way to access gold miners, the United Gold & General Fund (the “Fund”) offers direct exposure to the global gold mining sector.

The Fund invests mainly in gold miners (about 73 percent of the portfolio), complemented by select silver, platinum and industrial metals producers, providing broader opportunities across the metals and mining space. Top holdings include major industry names such as Newmont Corp and Gold Fields, giving investors exposure to established producers with scale and resilience.

Fig 3: Fund top 10 holdings, as of 31 Jan 2026

|

Name |

Weight (%) |

Description |

|

Gold Fields |

8.58 |

Global gold miner with assets in Africa, Australia, and the Americas |

|

Newmont Corp |

8.25 |

World’s leading gold producer with additional copper and silver operations |

|

Northern Star Resources |

6.22 |

Australian-based gold producer |

|

Evolution Mining |

5.23 |

Australian gold and copper producer |

|

Barrick Mining Corp |

4.07 |

Global gold and copper producer |

|

IAMGOLD Corp |

3.49 |

Canadian gold producer |

|

Alamos Gold |

3.16 |

Canadian gold miner |

|

Endeavour Mining |

3.09 |

Leading gold producer in West Africa |

|

Agnico Eagle Mine |

3.09 |

Canada's largest mining company and the second largest gold producer in the world |

|

Harmony Gold Mining |

3.21 |

South African gold miner |

Source: UOBAM, Morningstar, as of 31 Jan 2026

High return, high risk

The Fund has delivered strong results. As of 28 February 2026, the Fund is up 27 percent. And over the 1-year period, the Fund has posted an exceptional gain of 163 percent. This solid performance reflects the Fund’s exposure to high-quality miners and disciplined stock selection in the broader metals and mining sector.

However, the Fund’s high returns come with higher volatility. Its 3-year annualised standard deviation of 28 percent5 is well above the roughly 10 percent level typically seen in traditional equity funds. This elevated volatility underscores the Fund’s high-risk classification and the importance of understanding its risk–return profile before investing.

Fig 4: Fund returns as of 28 Feb 2026

|

|

Cumulative returns (%) |

Annualised returns (%) |

|

|

|

Year-to-date |

1-year |

3-year |

|

United Gold & General Fund |

27.05 |

163.35 |

50.60 |

Source: UOBAM, Morningstar, as of 28 Feb 2026. | Refers to United Gold & General Fund – Class A SGD Acc. Fund performance is calculated on a NAV to NAV basis, SGD basis, with dividends and distributions reinvested, if any. Performance figures for Year-to-Date show the percent change, while performance figures for 1 and 3 years show the average annual compounded returns. Past performance is not necessarily indicative of future performance. | Does not include the effect of the current subscription fee that is charged, which an investor might or might not pay.

The best of both worlds

For investors who prefer a balanced mix of gold exposures rather than relying on a single approach, UOB Asset Management also offers a blended solution. UOBAM Gold+, available on the UOBAM Invest app, combines the United Gold & General Fund and the SPDR Gold MiniShares Trust ETF in equal weights of 49 percent each, with the remaining allocation held in cash6. This gives investors exposure to both physical gold and gold mining stocks within one portfolio.

This structure positions investors to participate in gold price movements while also tapping into the growth potential of global mining companies, offering a more rounded way to invest in the gold theme.

1Source: Bloomberg, as of 4 March 2026

2Source: Bloomberg, as of 3 March 2026

3Source: World Gold Council, June 2025

4Source: World Gold Council, as of 28 Feb 2026

5Source: UOBAM, Morningstar, as of 28 Feb 2026

6Source: UOBAM, as of 19 Jan 2026

| If you are interested in investment opportunities related to the theme covered in this article, here are some UOB Asset Management funds to consider: United Gold & General Fund

UOBAM Gold+

|

MSCI Data are exclusive property of MSCI. MSCI Data are provided “as is”, MSCI bears no liability for or in connection with MSCI Data. MSCI full disclaimer at msci.com/notice-and-disclaimer-for-reporting-licenses.

This document is for general information only. It does not constitute an offer or solicitation to deal in units in the Fund (“Units”) or investment advice or recommendation and was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. The information is based on certain assumptions, information, and conditions available as at the date of this document and may be subject to change at any time without notice. No representation or promise as to the performance of the Fund or the return on your investment is made. Past performance of the Fund or UOB Asset Management Ltd (“UOBAM”) and any past performance, prediction, projection or forecast of the economic trends or securities market are not necessarily indicative of the future or likely performance of the Fund or UOBAM. The value of Units and the income from them, if any, may fall as well as rise, and is likely to have high volatility due to the investment policies and/or portfolio management techniques employed by the Fund. Investments in Units involve risks, including the possible loss of the principal amount invested, and are not obligations of, deposits in, or guaranteed or insured by United Overseas Bank Limited (“UOB”), UOBAM, or any of their subsidiary, associate, or affiliate (“UOB Group”) or distributors of the Fund. The Fund may use or invest in financial derivative instruments, and you should be aware of the risks associated with investments in financial derivative instruments which are described in the Fund’s prospectus. The UOB Group may have interests in the Units and may also perform or seek to perform brokering and other investment or securities-related services for the Fund. Investors should read the Fund’s prospectus, which is available and may be obtained from UOBAM or any of its appointed agents or distributors, before investing. You may wish to seek advice from a financial adviser before making a commitment to invest in any Units, and in the event that you choose not to do so, you should consider carefully whether the Fund is suitable for you. Applications for Units must be made on the application forms accompanying the Fund’s prospectus.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

UOB Asset Management Ltd Co. Reg. No. 198600120Z