Singapore is one of just 11 AAA-rated countries left in the world today. Coupled with the de-dollarisation trend and search for high-quality corporate bond yields, demand for SGD bonds looks set to persist over the long term.

Joyce Tan, Head of Fixed Income, Asia/Singapore

Making up for lost time

Unlike many other countries, in the 60 years since its independence, Singapore has largely managed to maintain annual budget surpluses, and has not needed to borrow money from investors to fund its expenditure.

As a result, Singapore came late to the fixed income game. The government only took concerted steps to build a liquid Singapore dollar bond market in 1997 following the Asian Financial Crisis. This development was driven, not simply by Singapore’s ambitions to be a regional financial hub, but also by a recognition that local corporations needed more diverse means of raising funds, including via bond issuances.

A vibrant corporate bond sector requires an equally vibrant government bond market. To achieve the latter, a weekly calendar of T-bill (Treasury bills) and SGS (Singapore Government Securities) issuances was created. Importantly, these had to be sizeable enough to support credible benchmarks and secondary trading activity.

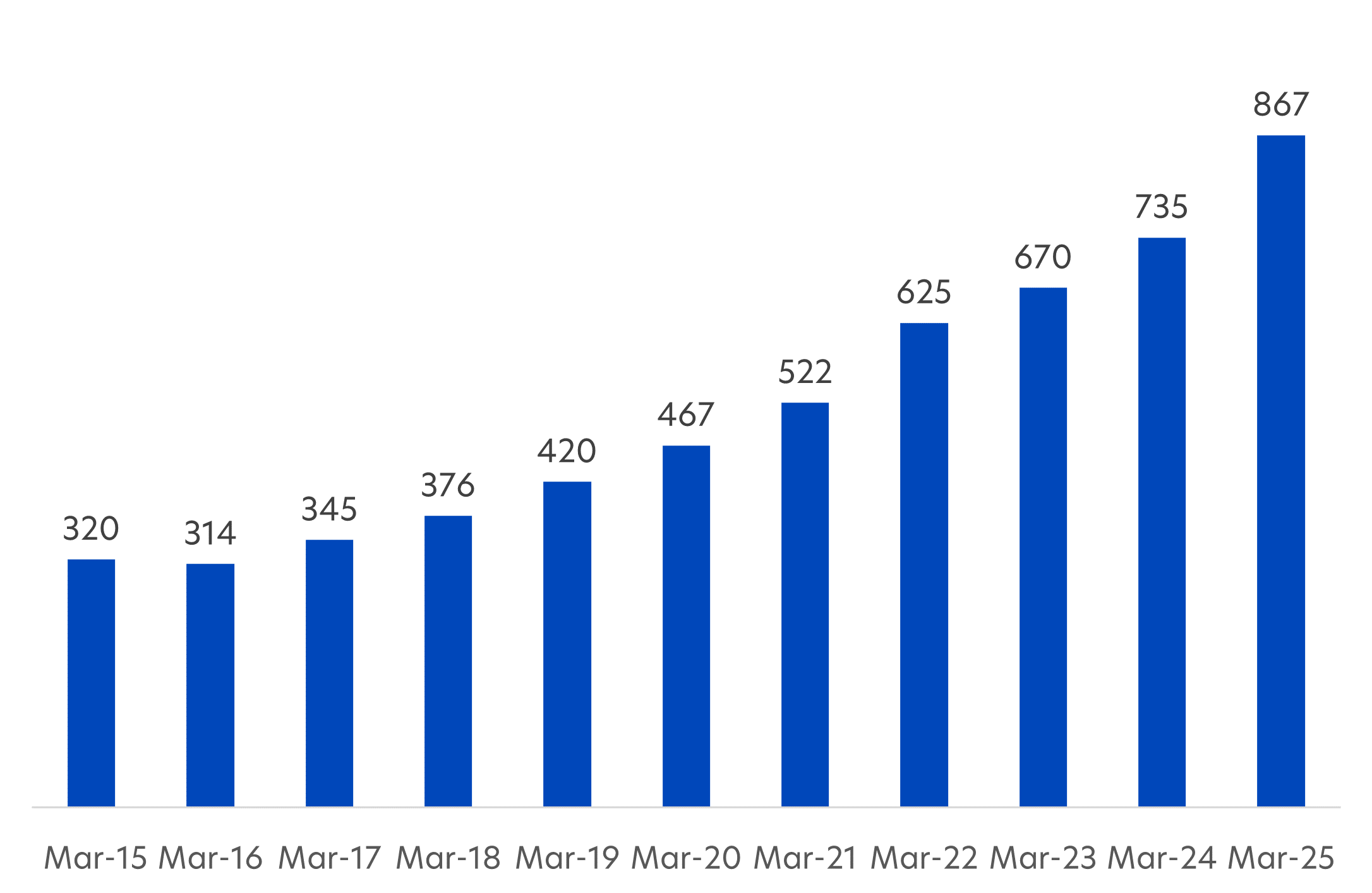

Since then, the Singapore bond market has gone from strength to strength. The stock of SGD bonds has risen from S$320 billion ten years ago to S$867 billion1 as of end-March 2025, an average annual growth rate of 10.5 percent.

Fig 1: SGD bond market size (S$ billions)

Source: AsianBondOnline/ UOBAM

Falling government bond yields

Today, government bonds comprise about three quarters of the SGD bond market. There were fears of over-supply when in November last year, the government sought to raise Singapore’s debt issuance ceiling by S$450 billion to S$1.515 trillion in order to fund specific long term development needs.

So far however, the supply of Singapore government bonds remains in line with historical trends. On the other hand, the demand for these bonds has picked up. Not only are Singapore’s AAA-rated government bonds regarded as a safe haven in an uncertain world, but the SGD is also benefiting from investors’ desire to be less USD-dependent.

This has resulted in a strengthening of the SGD and significant downward pressure on SGD bond yields. As an example, the yield on Singapore 6-month T-bills started the year at 2.9 percent, but has dropped to 1.7 percent as at 1 August. Over the same period, the SGD has strengthened by about 5 percent against the USD.

We expect this pressure on yields to ease slightly in 2H 2025 but not change course, given that the SGD is likely to stay firm although not appreciate much further from here. This is supported by the MAS’s decision last week to keep its monetary settings unchanged, and some analysts have even ruled out further easing in October.

More corporate bond opportunities

So what can investors do to offset the drop in Singapore government bond yields? One option is to extend the duration of your bond investments. However, longer-dated bonds have already seen price rises so far this year, and any further upside looks limited. Also these bonds tend to be more volatile because they are more sensitive to short-term interest rate movements. Therefore, investing in them requires a higher appetite for volatility.

A potentially better alternative is to capture opportunities within the corporate bond sector. Corporates tend to issue more bonds when interest rates are low because this allows them to reduce their funding costs while attracting interest from yield-seeking investors. There were 126 SGD-denominated corporate bond issuances in 2024 – the highest in a decade – and 60 in the first half of 2025, suggesting that the momentum is set to stay elevated.

The SGD corporate bond market also offers some specific advantages. It tends to be less volatile than USD markets, given differences in the way corporate bonds are valued and the Singapore market’s lower liquidity. Also, the majority of corporate issuers are statutory boards, established names in the domestic real estate or financial space, Temasek-linked entities and foreign financial issuers with high credit ratings. This mix helps keep default rates low.

Investors should note however that unlike government bonds, corporate bonds come with credit risk. Repayment on a corporate bond investment is subject to the issuer’s business fundamentals. As such, not all credits are created equal and investors are advised to be selective.

A recession hedge

Looking ahead, we note that the consequences of President Trump’s tariff policies may start to become more evident over the next few months, including the potential for a slowdown in global trade, higher US inflation, and diminished economic growth. Any potential retreat in the global risk sentiment will likely lend further support to the SGD bond market across all sectors as investors look to achieve above-inflation yields and positive returns at lower market risk.

1Source: AsianBondsOnline, March 2025

| If you are interested in investment opportunities related to the theme covered in this article, here is a UOB Asset Management Fund to consider: United SGD Fund

You may wish to seek advice from a financial adviser before making a commitment to invest in the above fund, and in the event that you choose not to do so, you should consider carefully whether the fund is suitable for you. |

All information in this publication is based upon certain assumptions and analysis of information available as at the date of the publication and reflects prevailing conditions and UOB Asset Management Ltd (“UOBAM”)'s views as of such date, all of which are subject to change at any time without notice. Although care has been taken to ensure the accuracy of information contained in this publication, UOBAM makes no representation or warranty of any kind, express, implied or statutory, and shall not be responsible or liable for the accuracy or completeness of the information.

Potential investors should read the prospectus of the fund(s) (the “Fund(s)”) which is available and may be obtained from UOBAM or any of its appointed distributors, before deciding whether to subscribe for or purchase units in the Fund(s). Returns on the units are not guaranteed. The value of the units and the income from them, if any, may fall as well as rise, and is likely to have high volatility due to the investment policies and/or portfolio management techniques employed by the Fund(s).

Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. An investment in the Fund(s) is subject to investment risks and foreign exchange risks, including the possible loss of the principal amount invested. Investors should consider carefully the risks of investing in the Fund(s) and may wish to seek advice from a financial adviser before making a commitment to invest in the Fund(s). Should you choose not to seek advice from a financial adviser, you should consider carefully whether the Fund(s) is suitable for you. Investors should note that the past performance of any investment product, manager, company, entity or UOBAM mentioned in this publication, and any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance of any investment product, manager, company, entity or UOBAM or the economy, stock market, bond market or economic trends of the markets. Nothing in this publication shall constitute a continuing representation or give rise to any implication that there has not been or that there will not be any change affecting the Funds. All subscription for the units in the Fund(s) must be made on the application forms accompanying the prospectus of that fund.

The above information is strictly for general information only and is not an offer, solicitation advice or recommendation to buy or sell any investment product or invest in any company. This publication should not be construed as accounting, legal, regulatory, tax, financial or other advice. Investments in unit trusts are not obligations of, deposits in, or guaranteed or insured by United Overseas Bank Limited, UOBAM, or any of their subsidiary, associate or affiliate or their distributors. The Fund(s) may use or invest in financial derivative instruments and you should be aware of the risks associated with investments in financial derivative instruments which are described in the Fund(s)’ prospectus.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

UOB Asset Management Ltd. Company Reg. No. 198600120Z