The next few years promise to be an exciting time for the Singapore equity market. In an early celebration of SG60, the Singapore stock market reached all-time highs over five consecutive days in July. We are optimistic that this momentum has room to continue, despite tougher days ahead.

Chong Jiun Yeh, Group Chief Investment Officer

60 years in the making

Singapore has moved from being a domestic to a regional financial hub in the 60 years since its independence. Financial services catering to local traders were already in place even in colonial times. However, the launch of the Asian Dollar Market and Asian Currency Unit in 1968 lay the foundations for Singapore’s modern financial industry.

These developments gave rise to the proliferation of domestic and regional financial institutions, which in turn led to the establishment of the Monetary Authority of Singapore (MAS) in 1971 as the country’s Central Bank and financial regulator. By the time the Singapore Exchange (SGX) was formed in 1999, Singapore was seen to be a well-regulated international financial centre able to support the listing, trading and settlement of key financial instruments including equities, fixed income, currencies, derivatives and commodities.

Singapore’s equity struggles

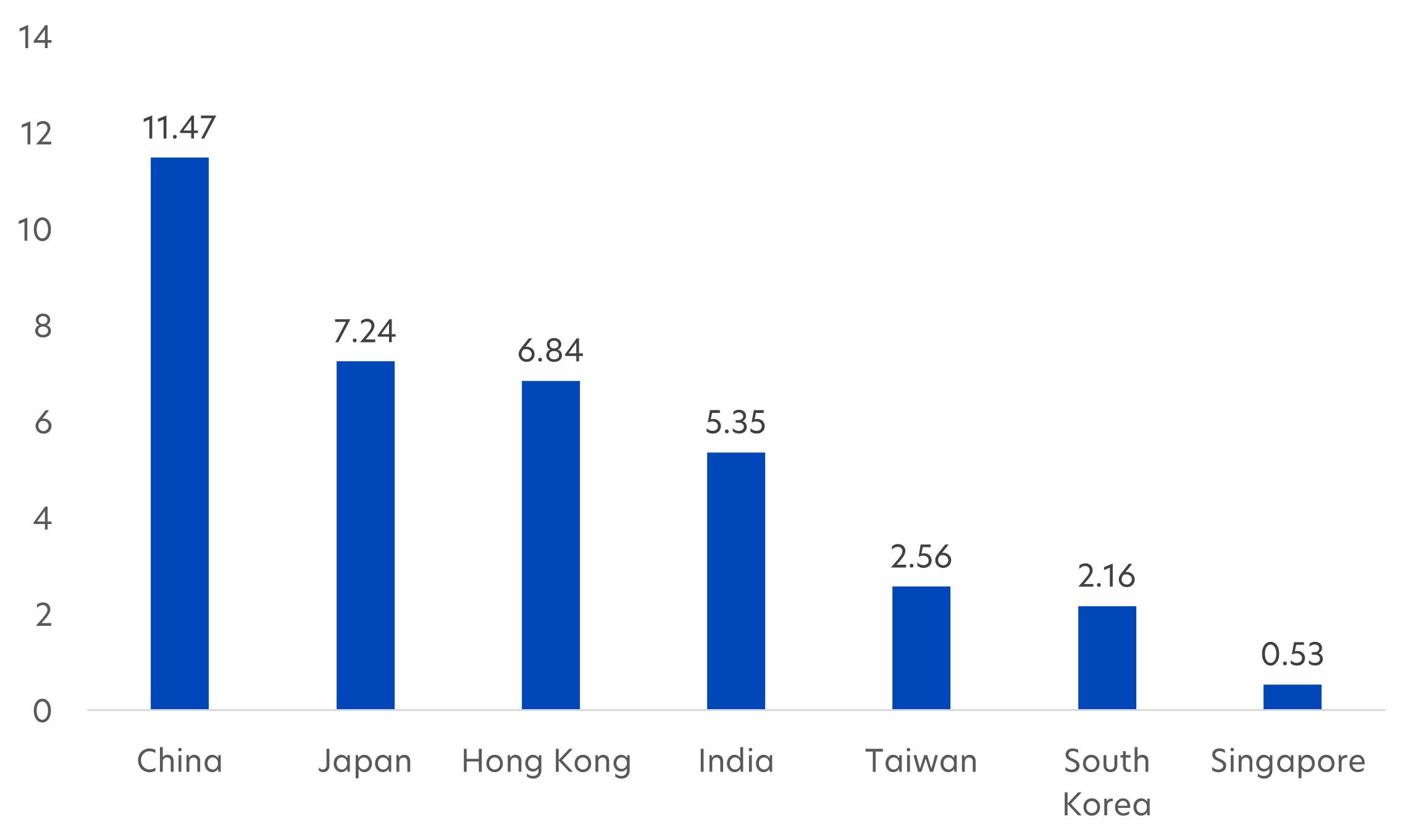

However, while Singapore still ranks high for currency and commodity trading, its equity market has fallen behind. With a market cap of S$532 billion1, the SGX ranks 23rd by market cap2 relative to other exchanges. In contrast, the Hong Kong Exchange (HKEX)’s market cap is more than 10 times larger3, despite its lower GDP.

Fig 1: Asian stock market capitalisation by country, US$ trillions

Source: Macromicro, July 2025

A vicious cycle has developed over time, given the twin evils of low liquidity and poor-quality listings. Over the past five years, the daily average trading volume on the SGX has been about 2.6 billion shares, significantly lower than the HKEX or the Taiwan Stock Exchange (TWSE).

Low investor participation meant that Singapore has struggled to attract new listings. In 2024, there were only four IPOs, all on the secondary Catalist market, collectively raising a mere S$31.4 million. The lack of stock market vibrancy depressed investor enthusiasm, with many institutional investors finding it expensive to execute trades, while the new generation of retail investors prefer to look to other stock exchanges, especially in the wake of easy-to-use digital trading platforms.

What has changed?

The Equity Market Development Programme (EQDP) was launched by the MAS and Financial Sector Development Fund in February 2025 to revive the Singapore stock market. It aims to do so in several ways, including making S$5 billion available to asset managers for investing in local stocks, simplifying the IPO listing process, and supporting smaller cap stocks beyond those listed on the Straits Times Index (STI).

Since its announcement, the Singapore stock market has been picking up steam. In the first half of 2025, the STI rose 19 percent ex-dividends, and 25 percent including dividends. This increase has been propelled by higher market activity, with June’s securities market turnover 23 percent higher than a year ago and the daily average value (SDAV) reaching S$1.3 billion, the highest in four years.

This investor pile-in continued in July with trading sessions this month registering S$1.5 billion or more. The naming of three asset managers - Avanda, Fullerton and JP Morgan – as recipients of the first S$1.1 billion tranche has helped keep the EQDP in the news.

Knock on effect from small cap boost

Despite the recent pickup in sentiment, many analysts remain guarded about its sustainability, pointing out that S$5 billion is only around 1.5 percent of the annual traded value of all stocks on SGX. Others are waiting for greater clarity on how the first tranche will be deployed and whether this will be enough to prompt high-quality listings over the longer term.

At UOBAM, we see the EQDP as a potential turning point in the Singapore stock market’s fortunes for three key reasons:

- The programme’s liquidity boost is sizeable in the context of small and mid-cap stocks. Historically, stocks with a market cap below S$5 billion account for about a third of SGX’s daily trades, so encouraging investor participation in this space can impact the entire market.

- We expect a net uplift of more than just the EQDP’s S$5 billion, given the higher churn rate for smaller stocks. As trading liquidity improves and research on small and mid-cap stocks broadens, we expect to see greater investor interest and the kick-starting of a positive share price discovery cycle.

- Addressing the liquidity problem can help reduce the Singapore market’s persistent discount relative to global developed markets. The P/E ratio for Singapore’s STI index has averaged 13 over the last 10 years, held back by Singapore’s low trading liquidity and lower ROE. The average P/E ratio for the S&P 500 over the same period is 18. Valuations on par with developed markets is seen as the missing piece needed to establish Singapore as a leading global financial hub.

Market strength in select sectors

In the near term, large cap stocks that have strongly outperformed so far this year could be subject to some investor profit-taking. However, we do not think that this will lead to a substantial pullback in the market. Stocks with strong fundamentals, a robust growth outlook and trading at reasonable valuations should continue to be well-owned.

Also, Singapore’s appeal as a safe haven within Asia, underpinned by a stable SGD, large and profitable banks, and healthy dividends yields currently averaging 5.3 percent, should continue to attract conservative investors. On top of this, investors with a higher risk appetite will help to support a small and mid-cap rally, especially those stocks with strong growth prospects and solid balance sheets.

Within this small and mid-cap space, a good management track record is key and investors will be seeking stocks that are trading at a substantial discount to their intrinsic value. Going forward, we will be particularly favouring those companies that can benefit from such imminent re-rating catalysts such as corporate restructuring, asset monetisation and capital management initiatives.

Growth slowdown

That said, we note that the MAS anticipates a slowdown in Singapore’s GDP growth trajectory as we move through the second half of the year, despite the unexpectedly strong 4.3 percent growth in 1H 2025. Although the US’s 10 percent tariff on Singapore exports is low compared to the other Asian countries, there is potential for widespread disruption to global trade and consumer demand.

As such, Singapore’s financial markets appear subject to opposing forces. On the one hand, investors have shown surprising confidence despite US tariffs, and have continued to push markets higher. On the other hand, any signs of slower growth in major economies could start to unnerve investors.

However, with inflation expected to stay low, the MAS will be keen to use all tools at its disposal, including further monetary easing, to help stabilise the economy and limit short term market volatility. Meanwhile, we would expect the EQDP to help provide a floor to the equities market over the longer term.

1Source: Macromicro, World total market capitalisation of stock markets

2Source: World Federation of Exchanges, Dec 2024

3Source: Macromicro, World total market capitalisation of stock markets

| If you are interested in investment opportunities related to the theme covered in this article, here are some UOB Asset Management Funds to consider: United SG Dynamic Income Fund

United Singapore Growth Fund

You may wish to seek advice from a financial adviser before making a commitment to invest in the above fund, and in the event that you choose not to do so, you should consider carefully whether the fund is suitable for you. |

All information in this publication is based upon certain assumptions and analysis of information available as at the date of the publication and reflects prevailing conditions and UOB Asset Management Ltd (“UOBAM”)'s views as of such date, all of which are subject to change at any time without notice. Although care has been taken to ensure the accuracy of information contained in this publication, UOBAM makes no representation or warranty of any kind, express, implied or statutory, and shall not be responsible or liable for the accuracy or completeness of the information.

Potential investors should read the prospectus of the fund(s) (the “Fund(s)”) which is available and may be obtained from UOBAM or any of its appointed distributors, before deciding whether to subscribe for or purchase units in the Fund(s). Returns on the units are not guaranteed. The value of the units and the income from them, if any, may fall as well as rise, and is likely to have high volatility due to the investment policies and/or portfolio management techniques employed by the Fund(s).

Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. An investment in the Fund(s) is subject to investment risks and foreign exchange risks, including the possible loss of the principal amount invested. Investors should consider carefully the risks of investing in the Fund(s) and may wish to seek advice from a financial adviser before making a commitment to invest in the Fund(s). Should you choose not to seek advice from a financial adviser, you should consider carefully whether the Fund(s) is suitable for you. Investors should note that the past performance of any investment product, manager, company, entity or UOBAM mentioned in this publication, and any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance of any investment product, manager, company, entity or UOBAM or the economy, stock market, bond market or economic trends of the markets. Nothing in this publication shall constitute a continuing representation or give rise to any implication that there has not been or that there will not be any change affecting the Funds. All subscription for the units in the Fund(s) must be made on the application forms accompanying the prospectus of that fund.

The above information is strictly for general information only and is not an offer, solicitation advice or recommendation to buy or sell any investment product or invest in any company. This publication should not be construed as accounting, legal, regulatory, tax, financial or other advice. Investments in unit trusts are not obligations of, deposits in, or guaranteed or insured by United Overseas Bank Limited, UOBAM, or any of their subsidiary, associate or affiliate or their distributors. The Fund(s) may use or invest in financial derivative instruments and you should be aware of the risks associated with investments in financial derivative instruments which are described in the Fund(s)’ prospectus.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

UOB Asset Management Ltd. Company Reg. No. 198600120Z