- Shares of US semiconductor companies like Intel fell sharply last week

- The industry has been suffering from high inventories and soft demand

- However, some segments of semiconductors are seeing restocking demand, suggesting that the worst may be over soon

- China’s industry looks set to benefit, despite its focus on older chip technologies

Disappointing earnings

Last Thursday semiconductor giant Intel reported that its fourth quarter revenues reached a mere US$14 billion. This was a third down from a year ago and one of the worst quarter’s performance in its history. The company’s full-year 2022 revenues of $63.1 billion was also 20 percent lower than a year ago.

Investors were disappointed and Intel shares sold down by close to 10 percent. The shares of other US chip companies, including Nvidia and AMD also fell, although less steeply.

Post-Covid blues

Intel and others in the semiconductor industry are suffering the effects of Covid-related adjustments. PC sales during the Covid lockdown were sky high, prompting PC manufacturers to hurriedly boost their chip inventories. So when the lockdowns ended, manufacturers simply tapped their bloated inventories, especially amid weakening sales.

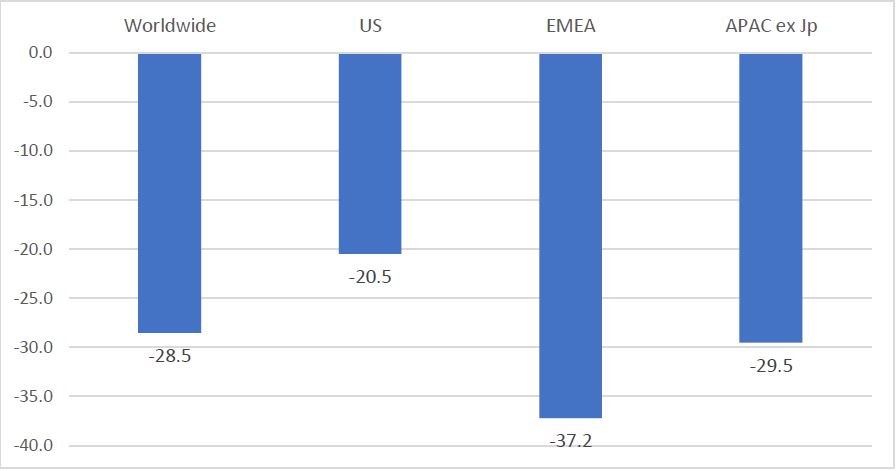

2022 saw sales fall further. Faced with high inflation, a possible recession and recent PC upgrades, consumers have stayed away. As a result, the fourth quarter of 2022 saw the weakest quarterly PC sales since the mid-1990s.

Figure 1: PC vendor unit shipment declines 4Q21 – 4Q22 (%)

Source: Gartner, January 2023

Fears of a global recession have also caused businesses to delay their data centre expansion plans. This post-Covid plummet in both consumer and business demand is undermining chip-makers’ profit margins. Intel’s profit margin reached a high of 59 percent in 2Q21, but this is expected to fall to 39 percent in 1Q23, according to company forecasts.

Gradual turnaround

However, these trends do not point to a long term structural decline and indeed, the green shoots of a recovery are starting to emerge. For example, the restocking of certain types of chips, such as Large-sized Display Driver ICs (LDDICs) used in TVs, notebook computers and desktop monitors, appears to be underway.

More advanced chips, such as ASICs (Application-Specific Integrated Circuits) are also seeing a faster recovery in demand, especially from recession-proof, deep tech industries such as defence, avionics and communication satellites.

All eyes are now on China. More cautious spending in the midst of the country’s zero-Covid policies had resulted in, for example, 286 million smartphones sold in 2022, the lowest in a decade. But alongside China’s reopening is also the likelihood of a consumption rebound, new model launches and meaningful restocking.

All this suggests that global chipmakers could see their revenues bottom out in 2Q23 and then pick up thereafter. With the end of the decline now in sight and valuations looking more attractive, we would expect this sector to see near-term investor interest.

US and China chip rivalries

This turnaround is particularly pertinent for China, given the country’s shift towards more manufacturing based technologies such as semiconductors. However, as highlighted previously, the US and China are locked in a chip war. Last year, the Biden administration announced controls on the export of advanced chip technologies to China and urged its allies and trade partners to do the same. This month, Japan and the Netherlands are thought to have signalled their intention to follow in the US‘s footsteps.

In response, China is working to establish a self-sufficient chip industry, and it was reported recently that a US$144 billion funding package has been created to support the country’s fledgling chipmakers.

China is playing the long game

While newer technologies are out of reach, these chipmakers are focused on accelerating the production of 28nm chips, which relies on a decade-old technology. For example, China’s largest chip manufacturer, SMIC, starting building four new facilities in 2020 and when completed, will have the capacity to triple their current production.

Given that 28nm chips still occupy over half of the global semiconductor market, the pending recovery will help boost the fortunes of the Chinese chip sector and buy it some time. A ready supply of locally-made chips will help to mitigate shortages as was experienced by China’s car and consumer electronic manufacturers in 2021. In the meantime, the same chipmakers will be racing to close the tech R&D gap with its global competitors.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

UOB Asset Management Ltd. Company Reg. No. 198600120Z