Key Highlights

- Global bond yields continue to rise as markets prepare for a global recession

- Short to mid-duration government bonds offer defensive properties

- USD strength is unlikely to ease in the short term

Central banks are tightening in unison

In a world that appears increasingly fractured, high inflation is a trend that is affecting almost all countries, big or small. As a result, the global inflation rate is forecast to average 7.4 percent for 2022, before easing to around 5 percent in 20231.

This would represent a near-doubling of the global five-year average inflation before the start of the pandemic, and is still a long way from the 2.0 percent target that most developed countries have in their sights.

Figure 1: Inflation rates across selected countries/regions

| Country/Region | Current rate (%) |

| UK | 9.9 |

| Euro Area | 9.1 |

| US | 8.3 |

| Singapore | 7.5 |

| Canada | 7.0 |

| India | 7.0 |

| South Korea | 5.7 |

| Japan | 3.0 |

| China | 2.5 |

Source: Trading Economics, Aug 2022

As a result, central banks globally have been tightening their monetary policies, whether in the form of higher interest rates, less government spending, or quantitative tightening (QT). In fact, according to the World Bank2, “Central banks around the world have been raising interest rates this year with a degree of synchronicity not seen over the past five decades”.

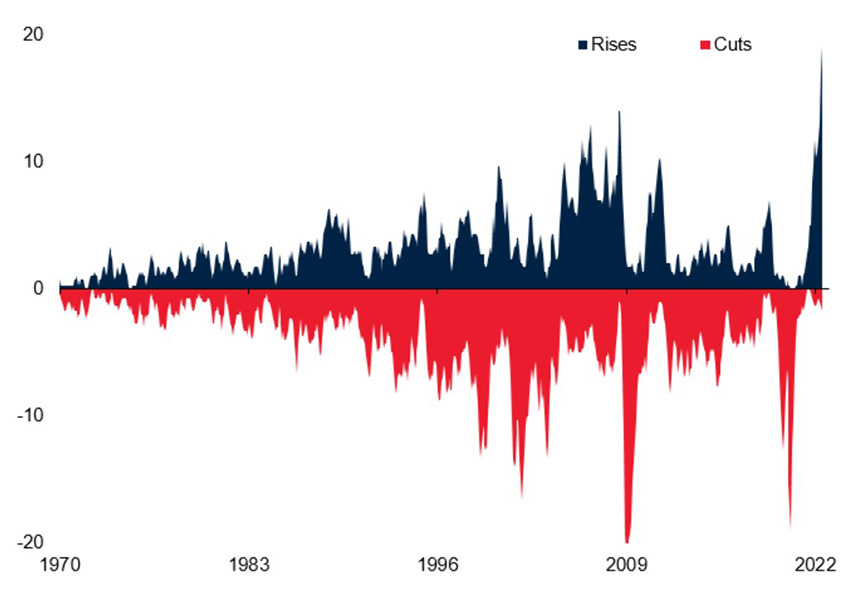

Figure 2: Global policy rate rises and cuts

Source: Bank for International Settlements, World Bank

Note: Three-month average of the number of policy rate rises and cuts over the month for 38 countries including euro area, July 2022

The has led to a sharp spike in the number of global policy rate rise events. Nor is the worst over. With global inflation stickier than most economists had expected, policy tightening is expected to extend into next year. Global rates are forecast to rise to almost 4 percent in 2023, close to double the level seen in 20213.

However, financial modelling by the World Bank suggests that this is still not enough and interest rates may need to rise by an additional two percent if countries want to hit their inflation targets. A large percentage of the world’s economies, both emerging and developed, are also tightening their fiscal stance, that is, raising taxes or cutting back on government spending. Given this level of central bank hawkishness in place across most countries, fears of a severe downturn in the global economy continues to mount.

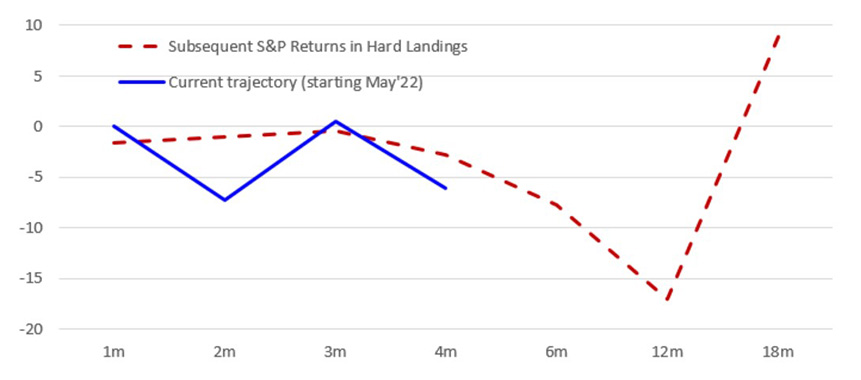

Equity markets tend to sell-off quickly in a hard landing

Hard landings are typically characterised by a marked slowdown in economic growth, high unemployment and lower company earnings. So how do markets behave in a hard landing scenario? Our study of previous recessions suggest that equity markets tend to correct by 20 percent or more. This can happen within a relatively short time frame of a year or less. Once at the bottom, equity markets tend to recover relatively quickly.

Figure 3: Expected trajectory in a hard landing

Source: UOBAM

Given that markets have already sold down by about 10 percent over the past four months in response to hard landing fears, we assess that we are about halfway through in terms of the potential price correction. Looking at the duration of the current correction cycle, we appear to be about a third of the way through compared to previous hard landings, which would suggest a market bottom in the second quarter of 2023.

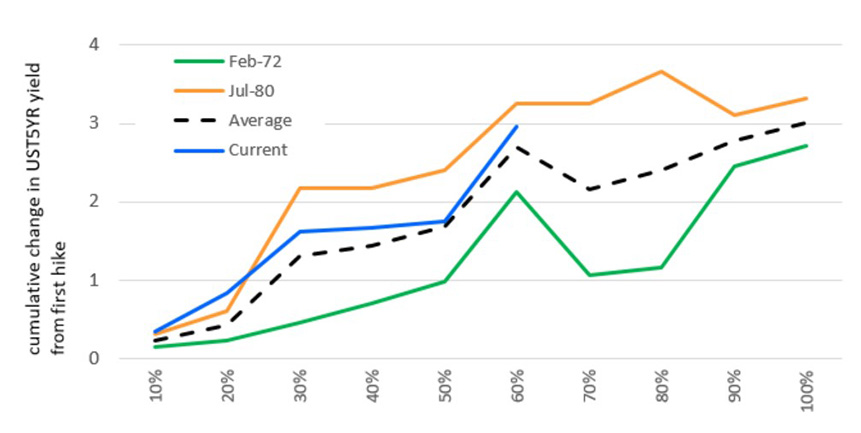

Bonds offer total return potential

Bond markets on the other hand, seem to take longer to fully sell down, typically two years or more. The current magnitude of tightening, supported by World Bank projections, indicate that central banks are about 60 percent into their rate hiking cycle, with another 40 percent of the cycle left to complete. In a hard landing, bond yields tend to peak only on completion of the hiking cycle, thereby suggesting a bottom in bond prices towards the third quarter of next year.

Figure 4: Change in bond yields across the rate hike cycle

Source: UOBAM

That said, bonds are already offering attractive yields. While a bottom may be several months away, bond prices look unlikely to fall much more from this point. The onset of a recession would tend to mark the easing off of central bank tightening. This would benefit bonds and especially high grade sovereign bonds and short duration high grade credits. These bonds are also likely to see higher demand as a hedge against equity market volatility. As such, on a total return basis, these bond assets offer a way to weather the current market volatility, even if economies tilt towards a deeper recession than had been expected.

1Statista, Global inflation rate from 2017 – 2027, Jul 2022

https://www.statista.com/statistics/256598/global-inflation-rate-compared-to-previous-year/

2;3World Bank Group, Is a global recession imminent, Sept 2022

https://openknowledge.worldbank.org/bitstream/handle/10986/38019/Global-Recession.pdf

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

UOB Asset Management Ltd. Company Reg. No. 198600120Z