Since the launch of ChatGPT, artificial intelligence (AI) has generated much investor enthusiasm. Tech companies have jumped on the bandwagon, rolling out AI chatbots and processing chips to capitalise on the surging demand for AI applications.

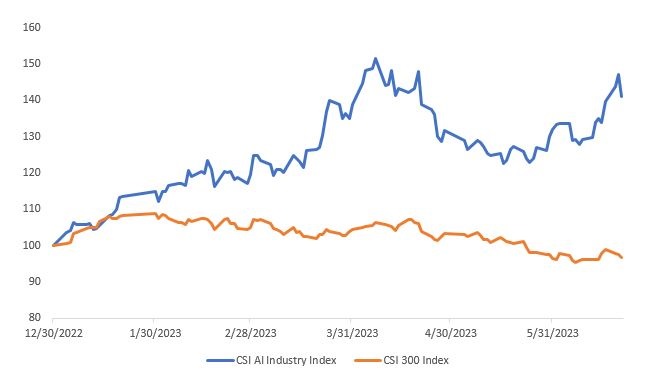

In China, the rush of interest has sparked a broad rally in AI stocks. The CSI AI Industry Index, which measures the performance of AI-related stocks in China, is up about 40 percent as of 21 June 2023, compared to the 4 percent decline in the benchmark CSI 300 Index.

Figure 1: CSI AI Industry Index vs CSI 300 Index, Jan – Jun 2023

Source: Bloomberg, performance as of 21 June 2023, in SGD terms

The sharp gains of several AI stocks even led China’s state media to call on regulators to curb potential speculation. While some valuations look stretched, we think there is still plenty of growth opportunities for China’s AI-related companies over the coming years, particularly in the hardware, software, and cloud computing sectors.

1. Hardware: China’s semiconductor supply chain industries

Semiconductors (known colloquially as chips) are necessary for the processing and storage of the massive datasets required for AI development. As AI applications such as ChatGPT become more popular, demand for AI chips is growing.

This represents an attractive opportunity for China’s AI-related semiconductor supply chains:

Foundries

Foundries are where semiconductors are fabricated based on specifications given to them by chip design companies. While Taiwan and South Korea still dominate the global market in foundries, China has been working to boost its own semiconductor production.

China’s two largest chipmakers, the state-backed Semiconductor Manufacturing International Corp (SMIC) and Hua Hong Semiconductor, currently rank among the world’s top 10 foundries by market share.

Figure 2: Top 10 foundries worldwide

| Ranking | Company | Market share (%) | Region |

| 1 | Taiwan Semiconductor Manufacturing Company (TSMC) | 60.1 | Taiwan |

| 2 | Samsung | 12.4 | Korea |

| 3 | GlobalFoundries | 6.6 | United States |

| 4 | United Microelectronics Corporation (UMC) | 6.4 | Taiwan |

| 5 | SMIC | 5.3 | China |

| 6 | HuaHong Group | 3.0 | China |

| 7 | Tower Semiconductor | 1.3 | Israel |

| 8 | Powerchip Semiconductor Manufacturing (PSMC) | 1.2 | Taiwan |

| 9 | Vanguard International Semiconductor Corporation (VIS) | 1.0 | Taiwan |

| 10 | DB Hitek | 0.8 | Korea |

Source: TrendForce, as of June 2023

There is potential for China’s foundries to serve the growing demand for AI chips given their capacity for large-scale production and China’s deep integration into global supply chains.

OEMs

Chinese semiconductor original equipment manufacturers (OEMs) are another potential beneficiary of rising AI chip demand. Such companies produce the tools necessary for chip fabrication, semiconductor testing and packaging.

In recent months, as global semiconductor OEMs withdrew part of their product offerings from the Chinese market amid US chip export restrictions, Chinese OEMs have stepped in to fill the gap – and seen significant revenue growth.

For the first quarter of 2023, the five largest listed Chinese OEMs reported revenue growth of 35 percent while the four largest global OEMs experienced a 28 percent contraction in the Chinese market1.

As US sanctions continue to bite, there is room for China’s OEMs to grow domestically and take market share from global chip equipment suppliers.

2. Software: Generative AI-enabled industrial solutions

The success of ChatGPT has prompted many global tech companies, including those in China, to develop their own generative AI technologies, particularly for enterprise use.

Baidu has secured sign ups from more than 650 companies to embed its AI chatbot, “Ernie Bot”, into their services. Alibaba has announced plans to launch cloud products and enterprise solutions based on its ChatGPT-like Tongyi Qianwen service, and integrate AI capabilities into its office collaboration platform DingTalk.

According to the Institute of Scientific and Technical Information of China (ISTIC), China’s generative AI applications have expanded to now include fields such as healthcare, the industrial sector and education.

This reflects China’s desire to promote the integration of AI and its economy, and opens up opportunities for Chinese tech companies to develop and apply generative AI tools to an even wider range of businesses and industries.

3. Cloud computing

Generative AI applications need tremendous computing power. For instance, companies working on AI development require significant cloud capacity to run generative AI workloads.

This is expected to drive new growth opportunities not just for China’s incumbent cloud service providers but also China’s telecom companies which are expanding into cloud computing infrastructure and AI software development.

For example, state-owned China Telecom, is set to be an up-and-coming player in China’s cloud market. The company plans to set up a new computing centre in Shanghai to support the city’s AI needs.

This investment comes as China seeks to boost its national computational power capabilities to accelerate domestic AI development. China currently accounts for 33 percent of the world’s computing power, which is only 1 percentage point lower than the US2.

More computing infrastructure support is in the pipeline. For instance, the Shenzhen local government recently announced it would set up a US$14 billion AI investment fund to scale up its computing power capabilities and become a pioneering AI hub in China.

Such developments offer Chinese telecom companies the opportunity to help build and operate China’s computing infrastructure over the next decades.

Risks to watch

Hardware, software, and cloud computing are poised to benefit from AI’s inevitable rise over the coming years. We believe China’s AI capabilities have the potential to expand over the longer term, given strong government support for continued AI development and China’s drive to gain self-sufficiency in key technologies such as semiconductors.

That said, the country faces challenges from the US’s chip export restrictions to China. Although Chinese companies are trying to design and produce AI chips domestically, their technologies are still lagging behind their foreign counterparts. The export rules are also likely to slow Chinese companies’ advances in AI as it restricts their access to high-end AI chips.

As it stands, many Chinese AI companies are still far from launching fully functioning generative AI products. The rally in AI-related stocks seems more driven by investor sentiment than company fundamentals. As a result, it could be susceptible to profit taking or any negative news.

1Source: Koyfin

2China Academy of Information and Communications Technology

If you are interested in investment opportunities related to the theme covered in this article, here is a UOB Asset Management Fund to consider:

|

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person.You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

UOB Asset Management Ltd. Company Reg. No. 198600120Z