Key Highlights

- Asian bonds appear to be gaining favour amid attractive valuations

- Investors are turning to bonds for yield and recession-hedging

- Chinese property bonds warrant continued caution, not yet time to bottom fish

Improved sentiment after a difficult first half

The Asian corporate bonds market rallied this past week. Since its low on 19 July 2022, the

J. P. Morgan Asia Credit Index (USD) has risen by close to 2.0 percent. This mirrors the price rises exhibited by global bonds and reflects investors’ relatively improved sentiment in Asia, plus a growing desire to add some protection to their portfolios in the event of an economic slowdown. At the same time, investors welcome the elevated yields, even for high grade, short-tenor bonds.

The uptick comes at the end of a steady downtrend that defined the first half of 2022. In the face of sticky inflationary pressures, steepening US interest rate hikes and a soaring USD, Asian investment grade and high yield credits weakened by around 10 to 15 percent respectively. During this period, new Asian bond issuances were at 10-year lows and June saw particularly high fund outflows from emerging Asian bond markets.

Long term support is becoming more evident

As such, whether the current rally is only a temporary blip or has staying power depends on the prevalence of a number of key factors:

1. Attractive valuations.

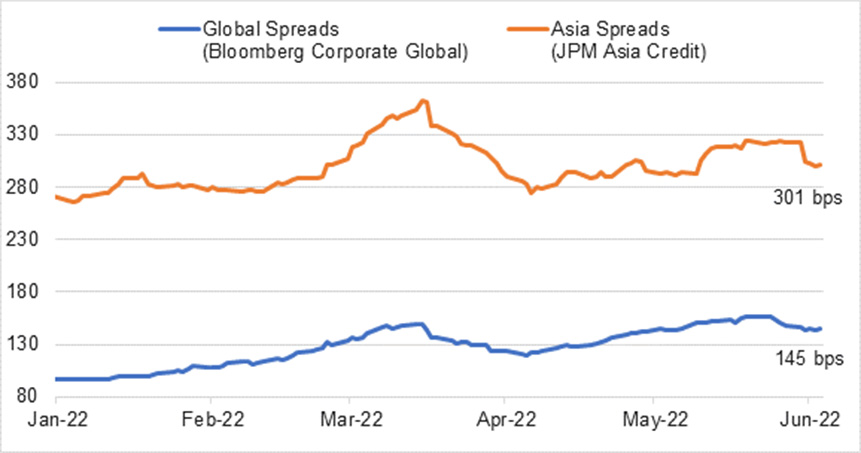

The yield offered by Asian corporates is typically in excess of US Treasuries due to their relatively higher risk. This yield pick-up, also known as spreads, is currently at around 300 basis points, more than double that of global corporates. In the face of the latest 75 basis points rate hike by the US Fed, Asian corporate bond spreads of expected to stay range bound. As a result, this sector should see good demand by those in search of yield,

Figure 1: Asia versus global credit spreads

Source: Bloomberg/UOBAM

2. Real Yields

Asian Investment Grade bonds are also offering real yields, that is high enough to offset the rise in inflation. Unlike some other emerging markets such as those in Latin America and EMEA, inflation rates in Asian countries like Malaysia and Indonesia are rising but still relatively low at 3.5 – 4.5 percent compared to potential credit yields Their role as commodity exporters are also helping to support growth and companies here may actually benefit from higher global price rises. If this real yield can be maintained, demand is likely to stay robust.

3. Sensitive to global trends

Many Asian countries also tend to be well-correlated to economic trends and sentiment within the wider global community. Countries like Korea and Taiwan are export-dependent, making them particularly sensitive to global developments. This means that any decline in US and European bond yields (and therefore higher bond prices) due to fears of an economic recession is likely to play out quickly in these Asian bonds. They therefore offer an effective way to hedge against a substantial decline in global risk sentiment over the coming months.

4. China’s selective outperformance

Within the emerging-market bond universe, Asian credit is generally regarded as higher-quality, given its potential for better risk-adjusted returns. Even during the Covid pandemic, some Asian credits were able to offer relatively high returns with less volatility. This is currently particularly true of selective China credit such as those within the infrastructure and utilities space. These sectors look likely to benefit from their strong policy mandate, and the fact that the country is loosening, rather than tightening, its monetary policy.

However, there is good reason to remain cautious of the Chinese property sector. We note that the widening of bonds spreads that has dominated the Chinese high yield property sector also affects high grade bond issuers. Even recent policy moves by the Chinese government in support of the local property market appears not to be having the desired impact. In particular, the publicity surrounding abandoned housing projects has dampened buyer enthusiasm and prolonged the weak demand. As such it is difficult to predict which Chinese property developers will still be standing at the end of the current crisis.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

UOB Asset Management Ltd. Company Reg. No. 198600120Z