UOB bank

The advent and development of artificial intelligence (AI) has altered the way companies interact with customers.

While banks’ traditional methods of dealing with customers involved mostly standardised offerings by way of a “transactional model”, customers now expect more tailored services in the new “engagement model”.

The age-old ways of communicating with customers include cold-calling, email campaigns with template offerings, reacting to issues after customers called the contact centre, and lengthy manual application processes.

In the new paradigm, customers expect their banking habits to be “remembered”, their needs to be anticipated, immediate response to queries, prompt advice on savings and investments, digitised on-boarding process and personalised recommendations.

To power this new customer journey, AI is increasingly being employed in banking and finance.

While much has been said about the benefits and promise of AI, there is varied understanding of what it really means. UOB’s Executive Director and Head of Group Enterprise AI, Data Management Office, Mr Johnson Poh, attempted to de-mystify the topic at a Masterclass following UOB Asset Management’s 2020 Investment Outlook Seminar.

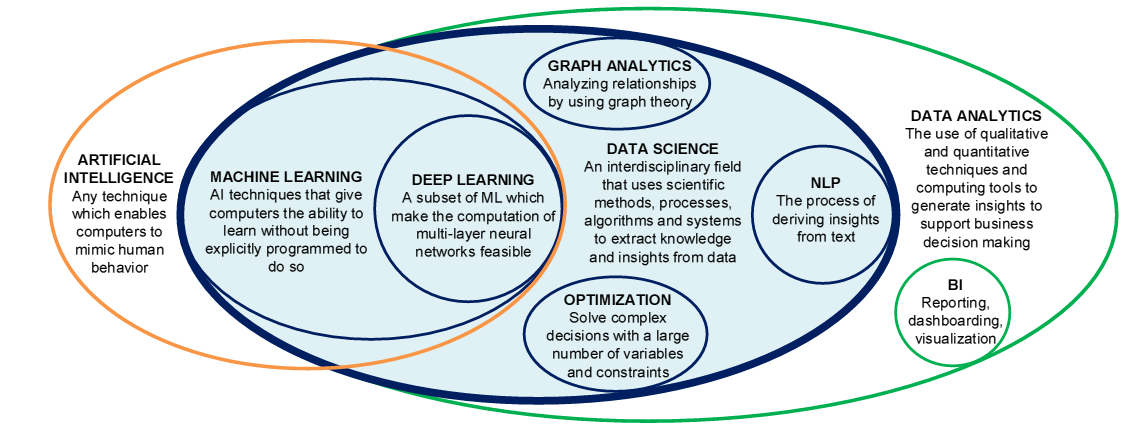

The definition of AI is broad – ranging from intelligent automation in its simplest form such as automating appliances in a home, to behaviour that mimics humans in its most complex manifestation such as developing self-driving cars.

The field of AI encompasses Machine Learning (ML), which is an AI technique that gives computers the ability to learn without being explicitly programmed to do so. Deep Learning (DL) is a subset of ML where the computation of multi-layered neural networks is made feasible, in an attempt to replicate the workings of a human brain.

Both ML and DL are also fields within Data Science and Data Analytics, where qualitative and quantitative techniques and computing tools are used to generate insights to support business decision-making.

Using the various facets of AI, ML and data analytics, each step of the customer journey can be enabled for a smoother ride. The key is in matching the right technology to the appropriate business use case.

The four main phases of the customer journey are:

Having identified the AI tools to adopt for each phase of the process, the next step is to figure out how to go about implementing them.

Mr Poh identified three key enablers:

With these three key enablers: people equipped with the expertise to drive processes and adopt the right technology, the AI tools can be implemented to better serve customers.

At the end of the day, with the use of AI to power business, customers will be able to benefit from improved engagement with a more seamless and pain-free experience. The use of AI in investment management can also potentially facilitate more dispassionate decision-making, which would ultimately produce better outcomes for investors.

Visit UOBAM.com.sg/perspectives/theyearahead.page for more on our 2020 outlook and insights.

Invest in your mind. Receive our curated insights in your inbox.

Subscribe