UOB bank

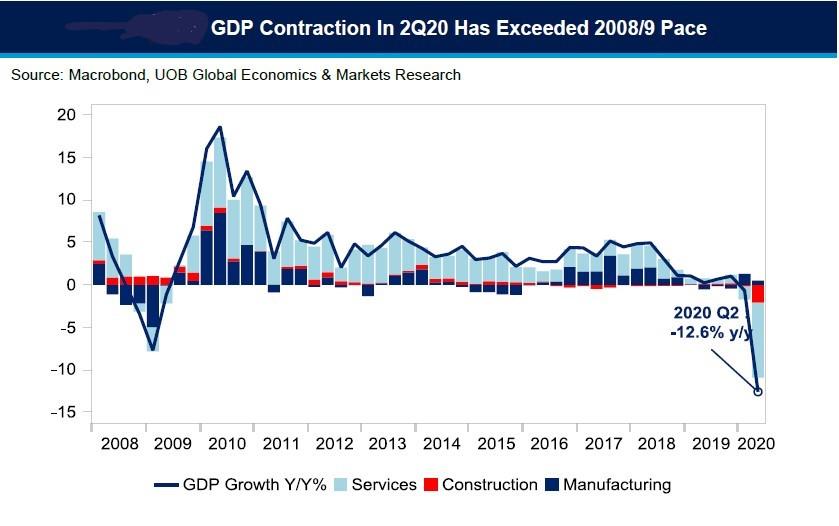

Based on advanced estimates, Singapore’s 2Q20 GDP had contracted by a record 12.6% year-on-year, marking its first technical recession since the first quarter of 2009. It is also the worst contraction on record outpacing market expectations for a 10.5% decline on year.

Outlook

Barring an unexpected upsurge in coronavirus (COVID-19) cases, the local economy should see a gradual pick-up in growth on the back of more business-friendly Phase Two and subsequently Phase Three measures. The opening up of tourist attractions from as of 1 July, coupled with more hospitality venues opening up to allow staycations, may be a first step to recovery in tourism-related sectors. However, a sustainable and robust recovery for related industries such as food and beverages, hotels and hospitality, transport and entertainment will still be dependent on the opening of Singapore’s borders to international visitors.

There still remains a high degree of uncertainty due to the unpredictable nature of the virus. Pharmaceutical exports only accounted for 9.9% of non-oil domestics exports (NODX) in 2019, while the biomedical manufacturing cluster weighed in just below 20% of total industrial production. This suggests that any exacerbation of the COVID-19 pandemic globally will likely be more detrimental than beneficial for Singapore’s manufacturing environment. Beyond the pandemic, other potential risks to growth disruption would be from brewing geopolitical flare-ups and trade tensions which may intensify in the second half of 2020.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The informationherein is given on a general basis without obligation and is strictly for information only. This publication is not an offer,solicitation, recommendation or advice to buy or sell any investment product, including any collective investmentschemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure theaccuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) andits employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decisionor action taken based on views expressed or information in this publication. The information contained in this publication,including any data, projections and underlying assumptions are based upon certain assumptions, managementforecasts and analysis of information available and reflects prevailing conditions and our views as of the date of thispublication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulaeor other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assistany person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAMdoes not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particularpurpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and otherforward-looking statement regarding future events or performance of, including but not limited to, countries, markets orcompanies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publicationconstitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specificobjectives, financial situation and particular needs of any specific person. You may wish to seek advice from aprofessional or an independent financial adviser about the issues discussed herein or before investing in any investmentor insurance product. Should you choose not to seek such advice, you should consider carefully whether the investmentor insurance product in question is suitable for you.

Invest in your mind. Receive our curated insights in your inbox.

Subscribe