UOB bank

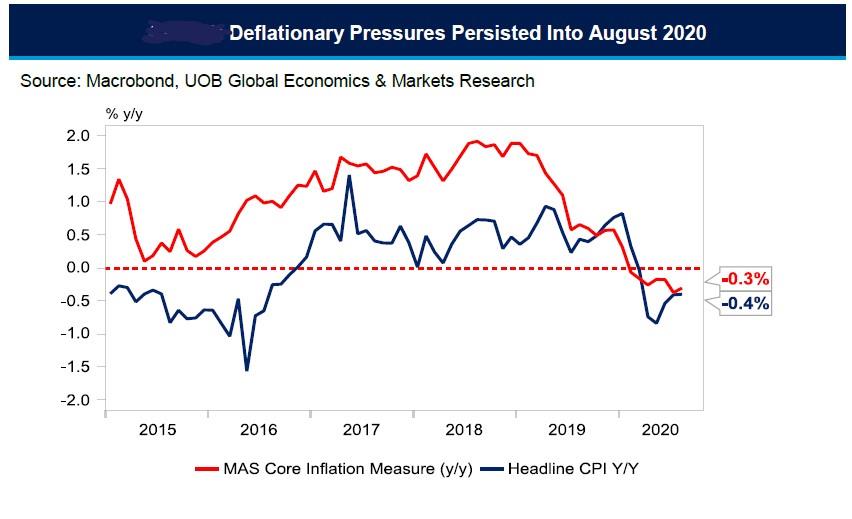

Singapore’s consumer prices fell 0.4% year-on-year (+0.6% month-on-month) in August, marking its sixth straight month of deflation. Core prices also declined 0.3% y/y though by a smaller contraction versus July’s -0.4% y/y.

The rate of deflation was slower compared to market expectations for headline CPI to fall by 0.5% y/y (+0.5% m/m) while core CPI was estimated to decline 0.4% y/y. Accounting for the latest data, consumer prices fell at an average pace of -0.2% in the first eight months of 2020, down from +0.6% over the same period last year.

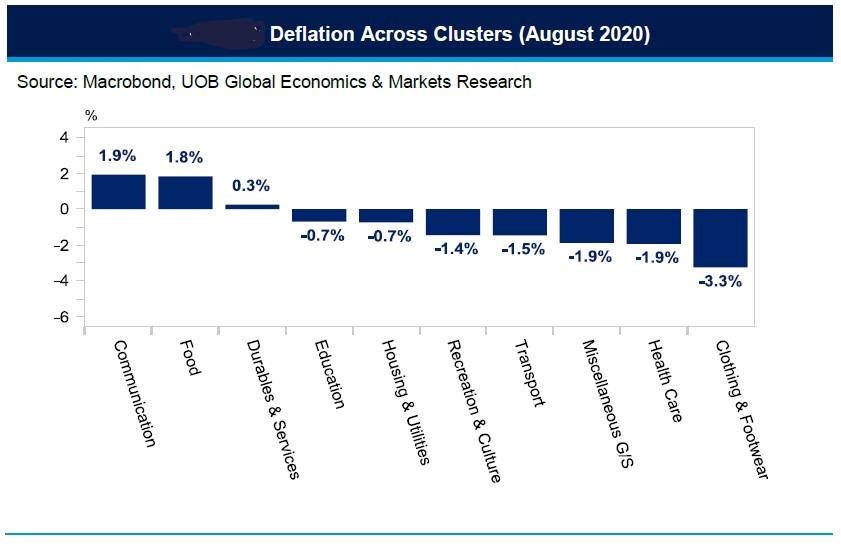

It was no surprise that deflation had persisted in August given lower oil prices amid lacklustre demand and a dearth in tourism spending. Clothing & footwear fell 3.3% y/y, marking its 17th straight month of contraction while transport prices for a fifth month running (-1.5% y/y) as Brent crude fell 22.9% y/y while COE premiums for vehicles softened 6.0% y/y in August 2020. Cost of electricity & gas continued to decline but at a slower rate given the easing in take-up of new subscriptions under the Open Electricity Market.

Higher food and communication prices

The overall decline in domestic consumer prices was cushioned by food and communication prices with food prices rising at its slowest pace in 5 months at +1.8% y/y in August, underlining the improving global supply conditions. Communication prices rose 1.9% y/y, clocking its fastest pace since April 2015, highlighting the increased demand for IT solutions and higher telecommunication services fees. Prices of household durables & services accelerated to +0.3% y/y in August 2020, up from +0.2% y/y the previous month.

The Monetary Authority of Singapore (MAS) and the Ministry of Trade and Industry (MTI) in their inflation report continued to highlight a “subdued” inflation outlook in 2020 noting that “external sources of inflation are likely to remain benign,” while lower oil prices will “weigh on the prices of energy-related components in the CPI basket.” Both are now of the view that “international food commodity price increases should generally be contained amid improved supply conditions.” The official outlook for both headline and core inflation remained unchanged at a range of between -1.0% and 0.0% for 2020.

Looking Ahead

Improving global supply conditions may cap the increase in food prices going forward while low oil prices will likely persist into 2020/2021, while relatively weaker labour conditions may dent domestic consumption demand. OPEC has revised its demand outlook for oil to an average of 90.2 (-0.4) million barrels per day (mbpd) and 96.9 mbpd for 2020 and 2021 respectively. The downgrade was in view of a faltering global economic recovery and tumbling fuel demand in the wake of the coronavirus pandemic. A negative impact on oil demand in Asia is expected to persist through the first six months of 2021.

Labour conditions are expected to weaken further into 2H20 following the gradual lifting of subsidies under the Job Support Scheme (JSS) into 4Q20. Wage subsidies for businesses at 75% (for the first S$4,600 of gross monthly wages between April-May 2020) will be lowered to 0% to 50% in 1Q21. Deputy Minister Heng Swee Keat, had noted in his statement on 17 August that retrenchments will be inevitable despite the government's best efforts.

We expect deflationary pressures to persist for the rest of this year

The mix of falling domestic and tourism-led demand, coupled with low oil prices for the rest of 2020 are formidable headwinds against consumer prices while the continued weak labour market should cap increases for discretionary goods and services demand. Improving supply conditions if they persist for the rest of this year should also cap increases in food prices. We are keeping our full-year headline and core inflation forecast at - 0.3% in 2020.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

Invest in your mind. Receive our curated insights in your inbox.

Subscribe