UOB bank

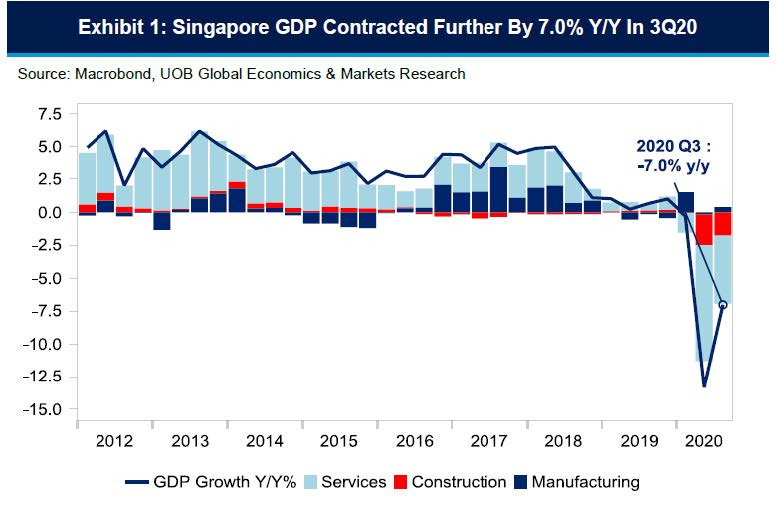

Singapore’s 3Q20 GDP contracted 7.0% year-on-year (+7.9 quarter-on-quarter, seasonally adjusted) according to advance estimates from the Ministry of Trade and Industry (MTI) versus market estimates of for a softer decline of 6.8% y/y (UOB estimate: -6.3% y/y). MTI has also lowered 2Q20 GDP growth to -13.3% from an earlier estimate of -13.2%. With the latest GDP print, Singapore’s economy fell by 6.9% in the first three quarters of 2020.

Despite the three consecutive quarters of contraction, the latest GDP print at -7.0% (+7.9% q/q sa) is significantly better compared to 2Q20 GDP at -13.3% y/y (-13.2% q/q sa) due to the phased re-opening of the economy after the Circuit Breaker from 7 April to 1 June 2020.

High-frequency data such as the Purchasing Managers’ Index (PMI), industrial production and non-oil domestic exports (NODX) point to continued progress. The September PMI data was relatively upbeat considering first-time expansion in new orders (50.1 points) in 8 months; faster rates of expansions in new exports (Sep 2020: 50.4 points vs Aug 50.2) and factory output (Sep: 50.8, Aug: 50.6). Manufacturing had expanded 13.7% y/y (+13.9% m/m sa) in August 2020, the fastest pace since March 2020 (+21.0% y/y) while NODX rose for the third straight month by 7.7% y/y in August. On a month-on-month seasonally adjusted basis, NODX grew by 10.5%, the strongest since April 2013 led by increase in both electronics exports (+5.7% y/y) and non-electronic exports (+8.3% y/y).

Decline led by construction and services sector

The construction sector fell 44.7% y/y in 3Q20 amid the slow resumption of construction activities amid reports of fresh COVID-19 infections in the foreign worker dormitories. The services sector contracted 8.0% y/y in 3Q20 vs 2Q20’s plunge of -13.6% y/y, as aviation and tourism-related sectors stayed lacklustre.

MTI noted that other trade-related services such as wholesale trade were “weighed down by weak external demand as major economies around the world continued to grapple with the COVID-19 pandemic.” The ministry also cited that other consumer-facing services sector such as retail and food services seeing “improvement in performance” but remain in contraction on a year-on-year basis. On a flipside, several sectors such as the finance & insurance and information & communication sectors continued to expand in 3Q20.

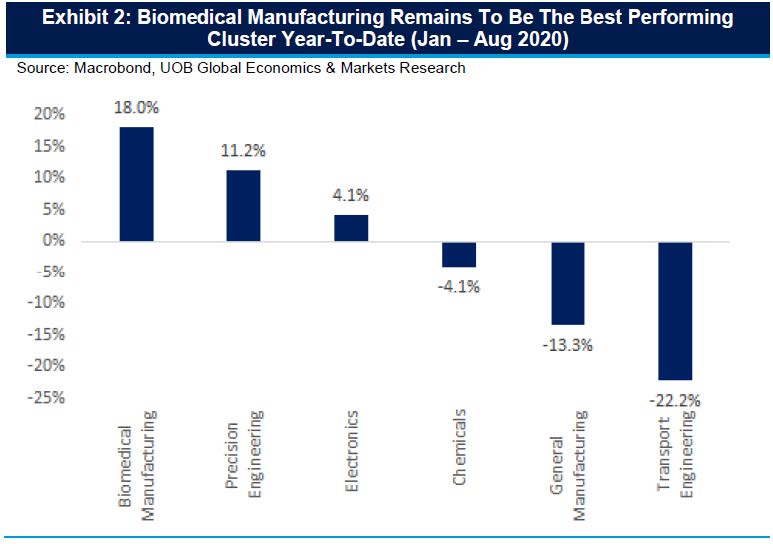

Bright spot

The manufacturing sector was a key bright spot, expanding at 2.0% y/y in 3Q20 and compared to a contraction of 0.8% y/y in 2Q20 led by output expansions in the electronics and precision engineering clusters and continued demand for biomedical products, digital solutions and semiconductor equipment. The biomedical manufacturing cluster is the best performing sector year-to-date given the higher export demand for medical instruments and high output of biological products.

Outlook

With the downside surprise in 3Q20 GDP of -7.0% y/y (+7.9% q/q sa), we expect 4Q20 GDP to weigh in at -5.2% y/y which will round up the full-year GDP growth to -6.5% in 2020, down from our initial outlook of -5.0%. Several bright spots such as the manufacturing sector amid improvements in Singapore’s high-frequency data further confirms that Singapore’s economy has been on the mend since the trough in 2Q20.

Based on the assumption that the pace of recovery can be sustained into 2021, we see growth likely weighing in at +5.0% in 2021, up from our prior outlook of +4.5%. Despite the recovery, real GDP in SGD terms will likely be lower than pre-COVID-19 levels. Our econometric models suggest that the pace of contraction in services and construction will decelerate further in the last quarter of 2020; while manufacturing growth in 4Q20 should improve due to a low-base print in 4Q19.

FX Outlook

Our view that is that USD/SGD will remain weighed by broad USD weakness. Easy monetary policy from the US Federal Reserve and the commitment to keep the Federal Funds Rate near zero under the new Average Inflation Targeting (AIT) regime will keep the USD weak. A strong CNY has also helped to anchor regional currencies, SGD included. As such, we continue to see further modest SGD gains against the USD, pushing USD/SGD lower to 1.35 by end 4Q20, 1.34 by end 1Q21 and 1.33 by end 2Q21.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

Invest in your mind. Receive our curated insights in your inbox.

Subscribe