Key Highlights

- Better-than-expected US inflation numbers have cheered global markets

- Recent global developments have added to the feel-good factor

- But sustained gains will depend on inflation continuing to ease at a good pace

- In the meantime, sovereign bonds show signs of resilience

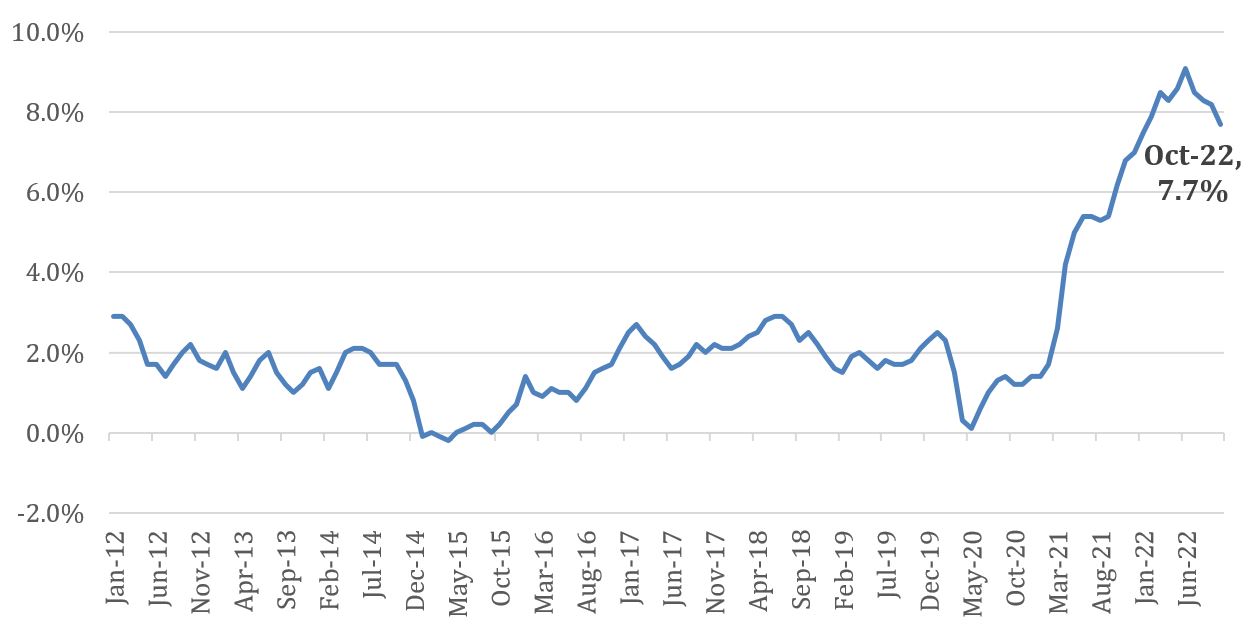

CPI strengthens hopes that US inflation has peaked

The US Consumer Price Index (CPI) for October helped to rally markets around the world. Not only did US consumer prices ease more than analysts were expecting, the trend suggests that inflation is no longer rising.

Figure 1: US Consumer Price Index All Items, 12-month percentage change, Jan 2012 – Oct 2022

Source: US Bureau of Labor Statistics

This news caused US markets to move up sharply, with the S&P500 jumping up nearly 6 percent in one day and 10 percent for the month (as of 10 November), although year-to-date the index is still down by 17.5 percent.

Asian stocks also rose immediately following the announcement, although in a more muted way, with rises of about 2 – 3 percent in Japanese, South Korean and Chinese indices. European markets also rallied with the pan-European Stoxx 600 up 2.8 percent that day.

Meanwhile, 2-year US Treasury bond yields fell to 4.34 percent from 4.61 percent the previous day. The hope is that the US Fed can now slow down its rate increases.

Recent developments also good news for markets

Alongside this moderation of inflation, several global events unfolding this week have been market positive.

- The Chinese authorities have also announced a 16-point plan to help stabilise the property sector and “optimise” current Covid restrictions.

- The US mid-term elections did not deliver the major disruptions that had been expected.

- Meanwhile the meeting between the US and Chinese President may not have resolved geopolitical tensions but seems to have helped dampen fears of a new Cold War.

- The Russia-Ukraine war appears to have entered a new phase with the retaking of Kherson suggesting that Russia may now be more accepting of managed withdrawals rather than fighting to the bitter end.

However, many uncertainties remain

While we are optimistic that the worst is over, and markets may stay buoyant for a while, there are also good reasons to anticipate more volatility:

- As the chart above shows, US inflation is still a long way from its historical average and the Fed’s two percent target. It is worth remembering that inflation is still rising, albeit at a slower pace than before. While core goods inflation is declining, core services inflation remains stubbornly high.

- From its 9.1 percent high in June, year-on-year inflation fell to 8.5 percent in July. But the drop in subsequent months was much smaller. Therefore, even if inflation has peaked, this only becomes meaningful when it is easing at a steady pace.

- After four consecutive 75 basis point Fed rate hikes, these latest CPI figures point to the possibility of a smaller hike in December. However, this is not guaranteed. By taking its feet off the pedal too early, Richmond Fed President Thomas Barkin warned recently that the Fed risks “inflation coming back even stronger”.

- The labour market is still tight and a recent report shows more jobs added in October than had been expected. This increases the risk of upside surprises in future CPI numbers, as was the case in six out of the last seven consensus forecasts.

- The Fed continues to walk the fine line between under-cooling and over-cooling the US economy. A few false moves by the Fed could push the US into a recession and it is still unclear at this point whether such a scenario can be avoided.

Sovereign bonds expected to be resilient

In the coming months, while economic growth data continues to beat expectations, we believe that there is room for growth prospects to deteriorate. This is because a hard landing view has not yet gained widespread acceptance and therefore has the potential to surprise.

For example, a Bloomberg poll of analysts found that opinion is divided - only 60 percent expect a US recession in the next one year. The relatively sanguine behaviour of equity and bond markets in recent months also suggest that they could be rocked by any growth surprises to the downside. If this happens, sovereign bonds look set to benefit from the flight to more defensive assets.

On the other hand, less defensive assets should benefit if growth prospects improve, inflation falls further, and the Fed adopts smaller rate hikes. But we would argue that much of this has already been priced in, limiting the potential gains.

Overall, high quality sovereign bond markets offer the prospect of price resilience, while staying attractive as a source of income and capital gains in the event of a recession.

China investments offer diversification benefits

In stark contrast to the rest of the world, China’s inflation in October grew by just 2.1 percent year-on-year, the lowest since April. In fact, the country’s producer price index (ie the prices that factors charge wholesalers) actually fell by 1.3 percent year-on-year. This disinflation is not surprising given that China’s domestic demand has been weighed down by Covid measures.

As we had forecast previously, any easing of the Covid rules would be warmly welcomed by residents and investors alike. And indeed, the announcement last week that some of China’s Covid restrictions were being relaxed was met with a rebound in Chinese stocks. Going forward, it is notable that the market forces behind the world’s top two economies are far from aligned. By investing in both the US and China, investors have the opportunity to achieve a high level of diversification.

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd (“UOBAM”) and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

UOB Asset Management Ltd. Company Reg. No. 198600120Z