UOB bank

The following paper “UIFT: Where to from here? – March 2022” is contributed by Wellington Management, the sub-manager of the United Income Focus Trust. All views expressed are based on available information as of the date of publication.

Amidst this challenging and uncertain market environment, we believe that UIFT can offer investors:

1. Genuine diversification across a range of asset classes

2. Dynamic asset allocation and risk mitigation controls

3. Focus on quality and liquidity with less sub-investment grade credit

4. The potential to confidently re-risk after a downturn and select attractive investment opportunities

Market complications piled up during the start the year, weighing on equity and bond returns. It all began with higher-than-expected inflation (US CPI hit 7.5% in January) and the Fed’s firm response (signalling a first interest rate hike in March). Then it took another turn with Russia’s invasion of Ukraine — creating a massive and distressing humanitarian crisis, while adding another layer of market complexity given Russia’s role as a global supplier of commodities. More recently, Wellington saw concerns over the Chinese economy/COVID-zero policy/dual listing policies, which further weighed on risk sentiment.

So where to from here? Wellington’s current base view is that we should expect a protracted conflict with little clarity on the “winner”, but with diminishing impacts on risk sentiment. Wellington thinks markets will continue to grapple with the trade-offs between inflation and growth and the central bank’s response. They remain convinced that inflation will be higher and stickier than expected. The war in Ukraine and sanctions on Russia only bolster this view, given the likelihood of additional supply-chain disruptions and shortages in agricultural, metal, and energy commodities. Higher energy prices could also weigh on growth.

In this challenging and uncertain market environment, we believe that UIFT can offer investors:

Genuine diversification across a range of asset classes: potentially providing resilience in volatile markets

Dynamic asset allocation and risk mitigation controls: Wellington’s active asset allocation process allows the portfolio to efficiently lean into the most attractive segments, while their robust risk management process helps protect the portfolio.

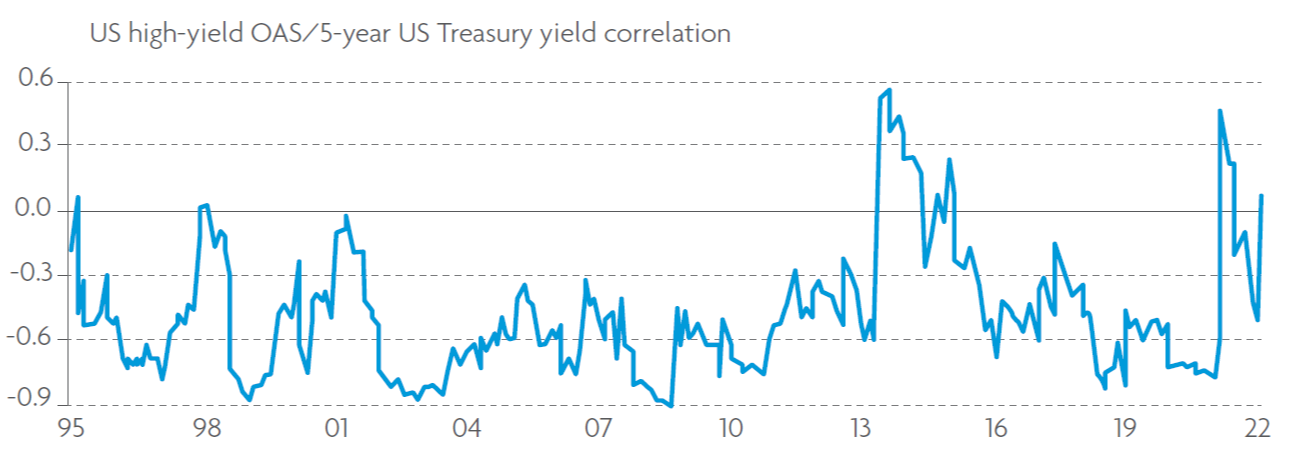

Source: Bloomberg | Chart data: January 1995 - February 2022

Focus on quality and liquidity with less sub-investment grade: As uncertainty persists, Wellington believes their focus on high quality and liquid instruments positions them well to navigate market volatility and capitalise on potential attractive opportunities to re-risk.

The potential to confidently re-risk after a downturn and select attractive investment opportunities

Below is a summary of Wellington’s latest multi-asset views over the next 6-12 months horizon:

| Asset Class | View | Change |

| Global Equities | Moderately OW | – |

| US | Moderately OW | ↑ |

| Europe | Moderately UW | ↓ |

| Japan | Moderately OW | – |

| Emerging markets | Moderately UW | – |

| Defensive Fixed Income | Moderately UW | ↑ |

| US Govt | Moderately UW | ↓ |

| European Govt | Neutral | ↑ |

| Japanese Govt | Moderately OW | – |

| Global IG Credit | Moderately OW | ↑ |

| Growth Fixed Income | Moderately UW | ↓ |

| High Yield | Neutral | ↑ |

| Emerging Market Debt | Neutral | ↓ |

OW = overweight. UW = underweight

Source: Wellington Management. Views have a 6 – 12 month horizon and are those of the authors and Wellington’s Investment Strategy Team. Views are as of 24 March 2022, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients. This material is not intended to constitute investment advice or an offer to sell, or the solicitation of an offer to purchase shares or other securities.,

This document shall not be copied, or relied upon by any person for whatever purpose. This document herein is given on a general basis without obligation and is strictly for information only. This document is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. The information contained in this document, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of the document, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product.

In preparing this document, UOBAM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was otherwise reviewed by UOBAM. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. UOBAM and its employees shall not be held liable for any decision or action taken based on the views expressed or information contained within this publication. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product is suitable for you.

Wellington Management is the sub-manager and sub-investment managers of the United Income Focus Trust. The views expressed here are those of Wellington Management’s portfolio manager(s) and should not be construed as investment advice. They are based on available information and are subject to change without notice. Portfolio positioning is at the discretion of the individual portfolio management teams; individual portfolio management teams may hold different views and may make different investment decisions for different clients or portfolios. This material and/or its contents are current at the time of writing and may not be reproduced or distributed in whole or in part, for any purpose, without the express written consent of Wellington Management. This advertisement has not been reviewed by the Monetary Authority of Singapore.

UOB Asset Management Ltd Co. Reg. No. 198600120Z

For queries on UOBAM's United Income Focus Trust

Contact us