You are now reading:

3Q26: 4 key themes as the clouds begin to clear

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

you are in UOB Asset Management![]()

You are now reading:

3Q26: 4 key themes as the clouds begin to clear

The first half of 2026 was marked by concerns over heightened geopolitical tensions, elevated energy prices and rising inflationary pressures. Yet, despite these headwinds, the global economy has proven remarkably resilient. As we enter the third quarter, many of the risks that dominated market narratives earlier in the year are beginning to moderate, setting up a more constructive outlook for investors.

Here are the four key themes shaping our views for 3Q26.

One of the most notable developments this year has been the strength of the global economy. Despite an energy shock stemming from the Middle East conflict, global growth has remained intact, corporate earnings continue to expand across major regions, and leading indicators still point to expansion rather than recession.

| GDP growth (%) | Earnings per share (EPS) growth (YoY%) | |||

| 2026E | 2027E | 2026E | 2027E | |

| US | 2.1 | 2.0 | 22.9 | 15.4 |

| Europe | 0.8 | 1.3 | 13.4 | 9.8 |

| Asia Ex Japan | 4.9 | 4.5 | 52.8 | 23.1 |

| China | 4.6 | 4.4 | 2.5 | 15.4 |

Source: Bloomberg, FactSet, UOBAM, as of 20 June 2026

Just as importantly, what were once headwinds are increasingly turning into tailwinds. Tariff-related headwinds are fading, oil prices have eased following the US-Iran interim peace agreement, and fiscal support in the US continues to provide a cushion for growth.

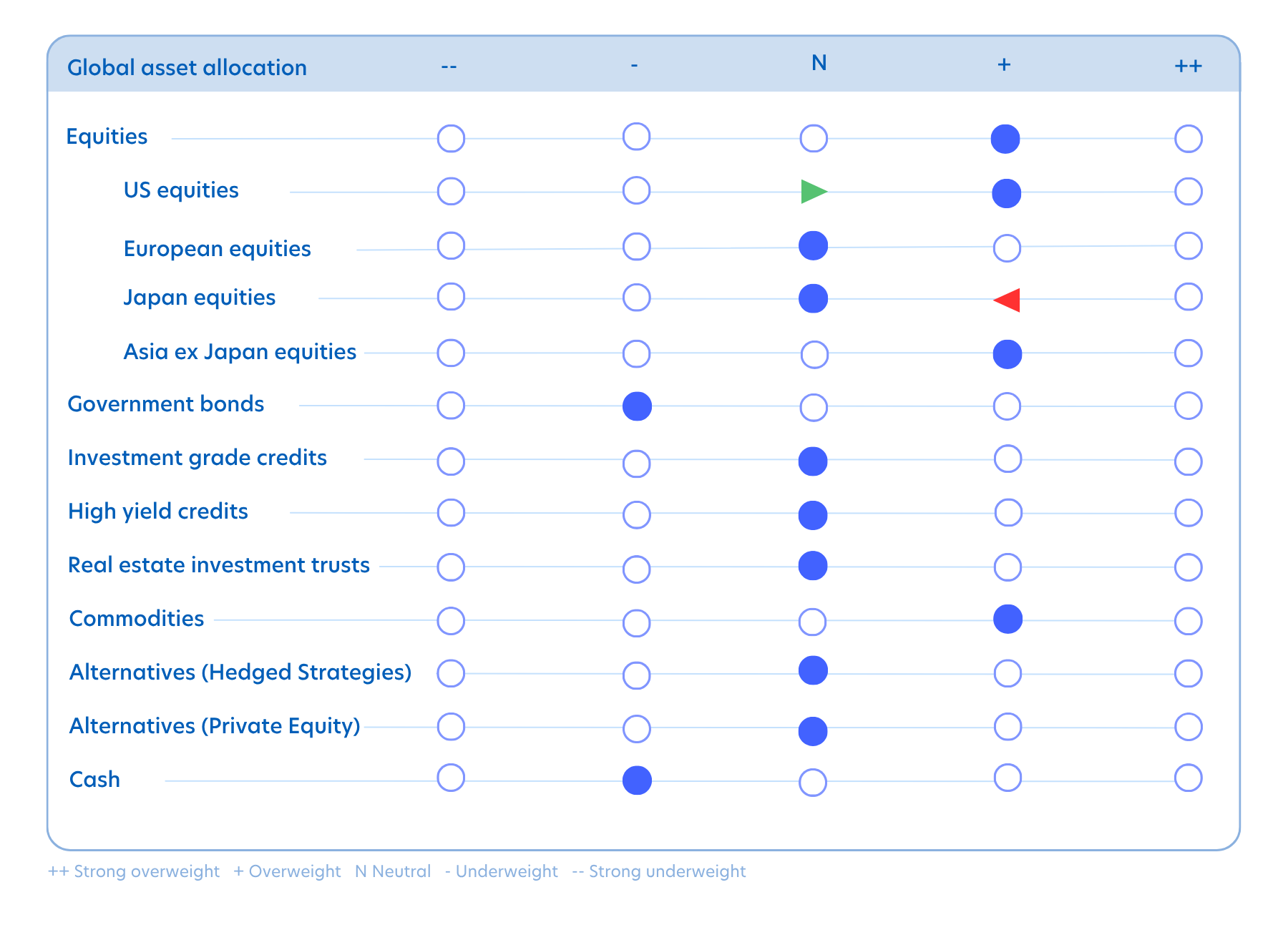

This improvement is reflected in our asset allocation views for the third quarter. We maintain an overweight position in equities, as resilient growth, healthy earnings and receding macro risks create a more supportive backdrop for risk assets.

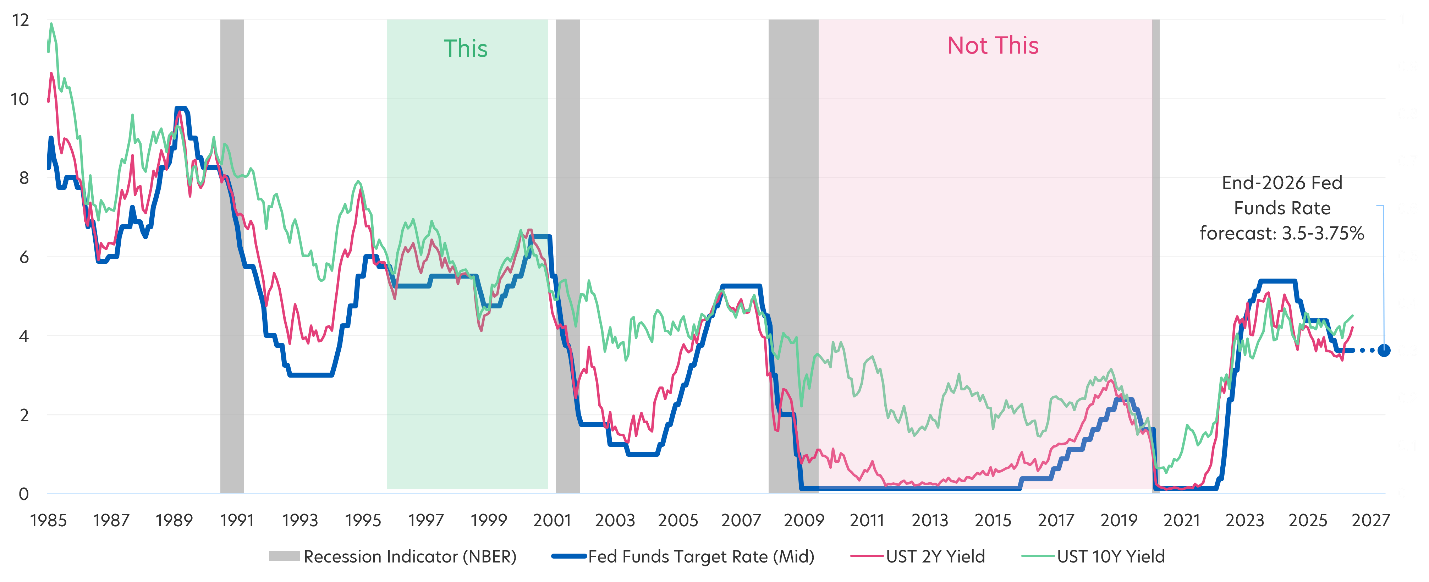

One of the key concerns facing investors today is whether elevated inflation will force the US Federal Reserve to hike interest rates. With inflation proving more persistent than expected, markets are now pricing in at least one rate hike by the end of the year, a stark reversal from the start of the year when investors were anticipating Fed rate cuts.

While the June FOMC meeting struck a more hawkish tone, we believe the Fed is more likely to remain on a prolonged pause rather than embark on a new rate-hiking cycle. In our view, inflation may remain sticky, but it is unlikely to reaccelerate meaningfully from here.

There are already signs that underlying price pressures are beginning to ease. Core goods inflation appears to have peaked, rental inflation is moderating, and wage growth is gradually slowing. Meanwhile, the recent easing in oil prices following the de-escalation of Middle East tensions should help alleviate some of the inflationary pressure seen earlier this year. Should price pressures continue to moderate as expected, the Fed could gradually shift towards a more neutral stance.

Our base case is therefore a higher-for-longer environment, but not a higher-and-higher environment. For investors, this should remain a relatively supportive backdrop for fixed income, with bond yields continuing to offer attractive income potential while the risk of materially higher rates appears limited.

Source: Bloomberg, UOBAM, as of 20 June 2026

One of our key calls for the third quarter is our upgrade of China equities from underweight to overweight. China is transitioning from a deflationary environment towards a more inflationary one — a development that is typically supportive of corporate profitability and earnings growth.

Moreover, the China story today is less about broad-based economic recovery and more about identifying pockets of strength. While headline economic data remains mixed, several sectors and regions continue to perform well, reflecting the uneven but ongoing rebalancing of the economy. Industrial profits are showing signs of improvement, and exports, which were a key growth driver last year, will likely remain an important source of support in 2026. While the broader property market is yet to see a turnaround, green shoots are visible in transaction volume and secondary market data.

We are also constructive on China’s innovation-led sectors. Areas linked to AI, semiconductors, advanced manufacturing, industrial technology and energy infrastructure continue to benefit from strong policy support and investment. These sectors are increasingly driving growth as China continues its shift towards a more innovation-led economy.

More broadly, we remain positive on Asia ex-Japan. The region continues to deliver some of the strongest growth prospects globally, while valuations remain at an attractive discount to US markets. As energy-related risks subside and earnings drivers broaden beyond tech, we believe the outlook for Asian equities remains compelling.

AI has been one of the defining investment themes of 2026. But increasingly, AI is becoming a macroeconomic story as well.

A key reason the global economy has remained resilient this year is the continued strength of AI investments. AI-related capex now contributes more to US GDP growth than the combined contribution of the automotive and housing sectors. Spending on AI infrastructure continues to accelerate, with AI-related capex estimated at US$380 billion in 2025 and hyperscaler investment expected to exceed US$525 billion in 2026. Importantly, much of this spending is committed over multiple years, providing a relatively durable source of growth even as other parts of the economy moderate.

Naturally, the strong performance of AI-related stocks has raised concerns that markets may be entering bubble territory. While pockets of exuberance exist, we believe the fundamentals are far stronger than in previous tech booms. Unlike the late-1990s internet bubble, where valuations surged despite limited profit growth, today's AI rally has been accompanied by substantial earnings growth. Corporate profits continue to rise even as corporate debt levels have declined, suggesting that the current cycle is being supported by genuine business fundamentals rather than debt-fuelled speculation.

While valuations warrant monitoring, history suggests that euphoric periods typically end with a meaningful economic downturn. Given resilient growth, improving inflation dynamics and moderating geopolitical risks, we do not currently see those conditions in place. In our view, the foundations underpinning this AI investment cycle remain considerably stronger than those seen in previous periods of market exuberance.

As we enter the third quarter, we believe the clouds that weighed on markets earlier in the year are beginning to clear. Growth remains resilient, inflation is likely to moderate, and the risks that investors worried about most at the start of the year have receded. Taken together, these developments support a more positive outlook for risk assets.

Against this backdrop, we maintain an overweight position in equities for 3Q26, with a preference for the US and Asia ex-Japan. While fixed income continues to offer attractive income opportunities, we see a more compelling risk-reward profile in equities and commodities, particularly gold and base metals.

Source: UOBAM, 20 June 2026. Note: *3-6 months horizon. The weights are relative to the appropriate benchmark(s), arrows show change from last quarter

02 Apr 2026 •