You are now reading:

COP27 opens new doors for investment

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

Tel:

• 6532 7988

Complaint Management

• Hotline: 1800 22 22 228

• Calling from overseas: +65 6222 2228

you are in UOB Asset Management![]()

You are now reading:

COP27 opens new doors for investment

After 14 days of heated debate, discussion and wrangling, here are the key global takeaways:

Progress made by Asian countries

Asian countries achieved some important milestones as part of COP27 discussions.

Firstly, multilateral development banks will help provide financing for countries and companies to wind down and retire coal plants and advance investments to renewables. This includes Asian Development Bank’s Energy Transition Mechanism (ETM), which seeks to retire existing coal-fired power plants on an accelerated schedule and replace them with clean power capacity. Countries are also coming together to create partnerships. This includes the US-Indonesia climate finance deal which provides $20 billion for Indonesia to pivot away from coal and Vietnam's announced Just Energy Transition Partnership.

Secondly, Singapore, Vietnam, the Philippines and Indonesia are among the 150 signatories of the Global Methane Pledge (GMP), which aims to cut methane emissions by at least 30 percent by 2030. While China – one of the largest methane emitters – has not signed the pledge, it has drafted a national plan to curb methane emissions.

Thirdly, Singapore is establishing several carbon market agreements with other countries, and has already set up one with Papua New Guinea. Singapore is also discussing similar trade deals with 20 other countries, and have signed agreements with Vietnam, Morocco, Thailand, Ghana and Colombia.

Investment opportunities to look out for in Asia

The two-pronged approach for tackling climate change – mitigation and adaptation – provide some clear investment outcomes for Asian countries.

Mitigation is the reduction of emissions and stabilization of levels of heat-trapping greenhouse gases in the atmosphere, through reducing sources of these gases and enhancing the ‘sinks’ that accumulate and store these gases (e.g. oceans, forests and soil). Several investment opportunities arise from mitigation strategies ie

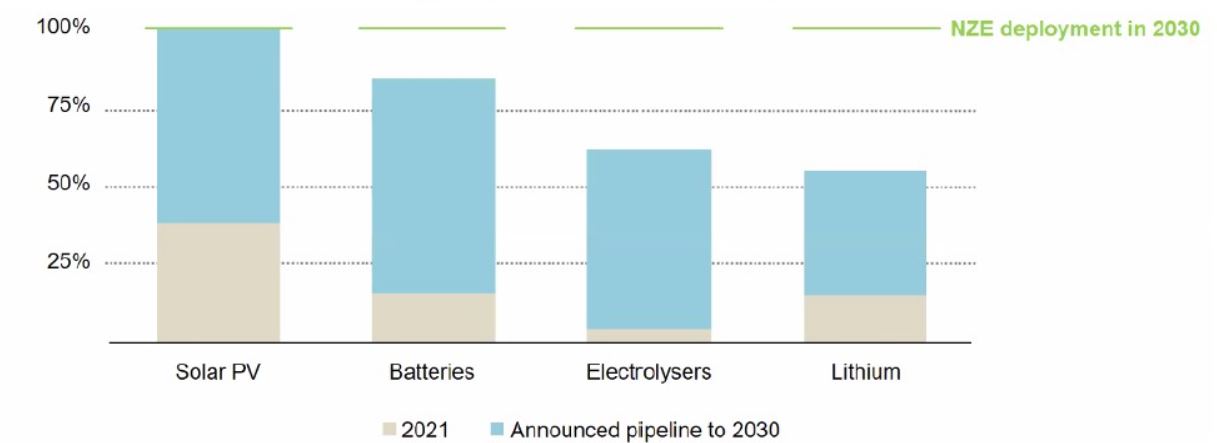

Figure 1: Manufacturing capacity in 2021 vs required capacity in 2030

Source: IEA

Clean energy manufacturers have also announced aggressive pipelines to scale up manufacturing capacity. In addition, Singapore and Cambodia signed a memorandum of understanding in September to deepen cooperation on clean energy transition, which will help facilitate the development of regional power grids and cross-border grid interconnections for electricity between both countries.

Source: UOBAM

Adaptation to climate change includes building a resilient society that allows companies to bounce back through building infrastructure that can withstand extreme weather events. Implementing early warning systems can also help to evacuate areas prone to extreme weather. Several investment opportunities arise from adaptation strategies ie

These adaptation strategies would normally be supported by innovative technology, disaster management and infrastructure upgrades, which are promising themes that can be considered for investment.

Stranded risks increase for companies unable to transition

Along with the opportunities are also the risks especially to companies and sectors unable to achieve the required transition. Value at risk is a measure of risk of loss for an investment and this tends to have a strong correlation with the average sector emissions intensity.

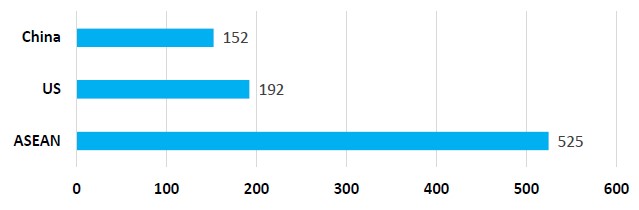

By using a fair-share production approach to estimation, estimated methane emissions were attributed to companies. In particular, ASEAN stands out significantly in terms of its current methane emissions intensity when compared to the US and China. The average methane emissions intensity shows how much methane is emitted by companies in the region, divided by revenue and shows that ASEAN’s intensity is more than triple that of China’s.

Figure 2: Estimated Average Methane Emissions Intensity (CH4 tonnes/million USD)

Source: UOBAM, Climate Trace, IEA

Value-at-risk is a measure of risk of loss for an investment and this tends to have a strong correlation with the average sector emissions intensity. Companies with high methane intensity therefore stand to have a higher value-at-risk, something that the UOBAM Sustainability Office will be keeping a close eye on.

Despite China’s lower methane intensity expected expansion of its national Emissions Trading Scheme by 2025, especially for the eight hard-to-abate sectors, could impact certain power, iron and steel, and building materials companies.

Also China, along with South Korea and Taiwan, are home to some of the largest operational coal plants in the world. These are set to become obsolete as the world moves towards its net zero goals. The estimated global net present value of stranded assets in coal power generation through to 2050 ranges from $1.3 to $2.3 trillion. However, there remains a lack of energy transition mechanisms in countries with significant coal assets. By not adequately addressing the problem of divesting or retiring these coal assets, the risk of stranded assets increases.