Supported by a stronger SGD, safe haven demand and a resilient rates backdrop, Singapore bonds are well‑placed to hold up better than global bond markets in the months ahead

Edward Ng

Portfolio Manager, Macro Strategy & Multi-Asset

The war in Iran has pushed global oil prices above US$100 per barrel multiple times since March, roiling energy markets and raising global inflation risks. As a small, open economy that imports almost all of its energy needs, Singapore is especially exposed.

Higher energy prices tend to filter quickly into Singapore’s economy. Roughly 8 percent of Singapore’s CPI basket is directly sensitive to energy-related components such as electricity, gas, petrol, transport and airfares. Higher fuel and utility costs also raise business, logistics and supply‑chain expenses, creating a broader second‑round impact on consumer prices.

With Singapore’s core inflation climbing to a 14-month high in February, price risks are now skewed to the upside. MAS has already indicated that Singapore’s inflation outlook will be reassessed at the upcoming April policy meeting, citing a “significant” rise in import cost pressures linked to the Middle East conflict.

SGD set to strengthen further

Against this backdrop, the likelihood of MAS tightening monetary policy at the next review has increased substantially. Unlike most central banks that fight inflation by adjusting domestic interest rates, MAS does so by managing the Singapore dollar nominal effective exchange rate (SGD NEER). When inflation risks rise, MAS typically tightens policy by allowing the SGD to appreciate more rapidly against a basket of currencies from Singapore’s major trading partners.

Historically, periods of rising energy prices have coincided with a stronger SGD NEER, reflecting MAS’s preference for using currency strength to counter imported inflation. A firmer SGD makes foreign goods, including oil and other commodities, cheaper in local currency terms, helping to offset part of the global cost surge.

Given the current inflation risks stemming from elevated oil prices, MAS is therefore likely to tighten policy sooner rather than later, providing further support for the SGD. In fact, the SGD has been one of Asia’s strongest performers this year, supported by a combination of safe haven inflows and market expectations of MAS tightening.

Impact on SGD rates

A tighter MAS stance also means domestic interest rates are unlikely to continue falling. SGD interest rates (such as SORA, the benchmark for most Singapore home loans) had been steadily declining over the past year as core inflation eased. But this trend may reverse as markets price in renewed inflationary pressure, with Singapore rates across various tenors stabilising and even starting to edge higher in recent weeks.

Historically, whenever core inflation rises and MAS adopts a tighter policy, SGD interest rates tend to remain firm or drift higher, in line with an appreciating SGD NEER path. This is because allowing SGD rates to fall too much would risk loosening financial conditions at a time when MAS is trying to curb imported inflation. As a result, if inflation risks remain elevated, we could see SGD interest rates stay at relatively higher levels in the months ahead.

Singapore bonds back in the spotlight

So, what do a stronger Singapore dollar and firmer SGD interest rates mean for investors? Together, they create a materially improved backdrop for Singapore government bonds and high‑grade SGD corporate bonds, placing Singapore bonds back in focus.

1. Currency strength cushions volatility

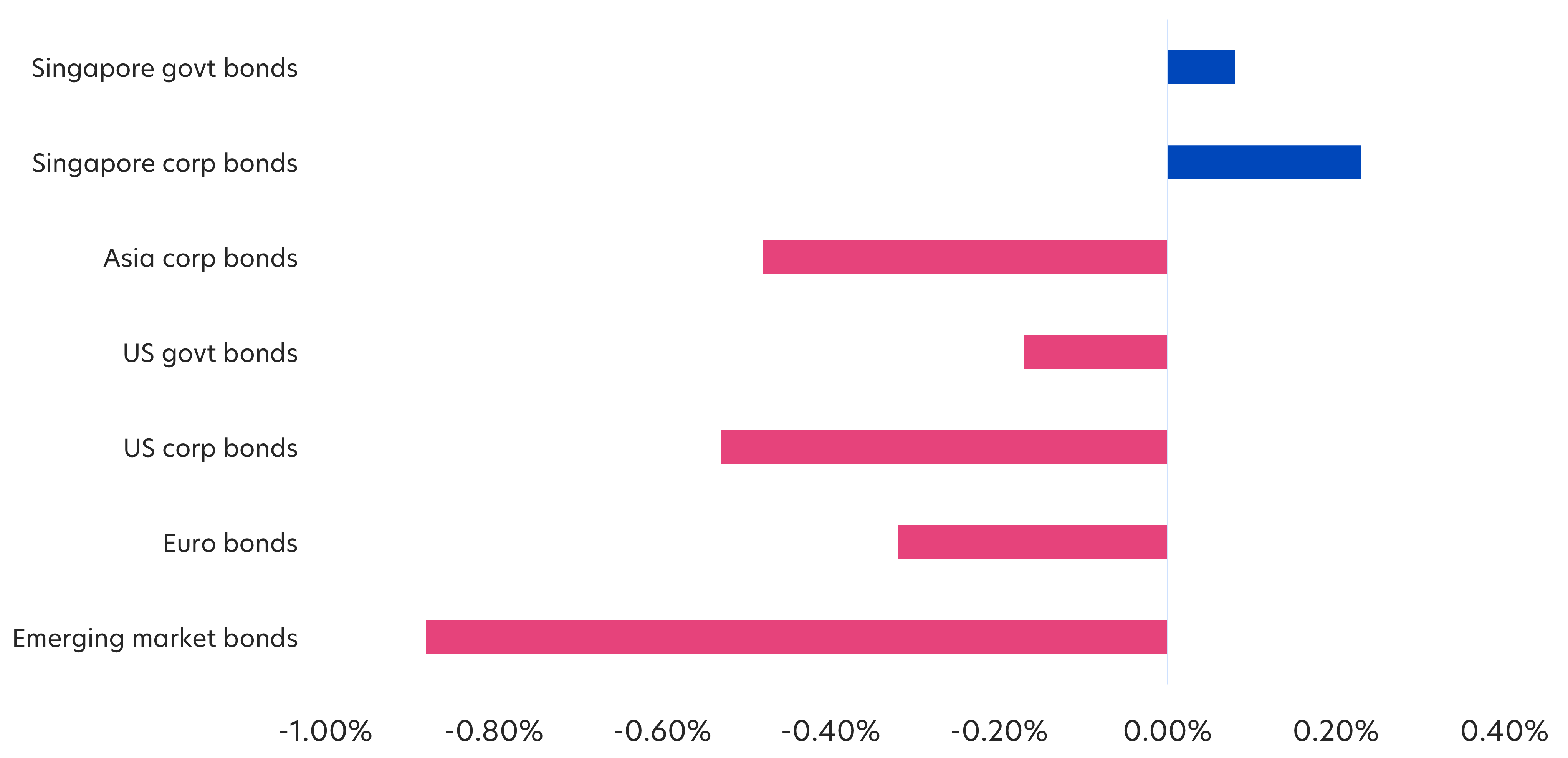

Singapore bonds have demonstrated notable resilience so far this year, outperforming most other bond markets, including US bonds.

Fig 1: Singapore bonds have held up well YTD

Source: Bloomberg, as of 25 March 2026. SG govt bonds: Markit iBoxx ALBI Singapore Govt TRI, SG corp bonds: Markit iBoxx SGD Corporates Index TRI, Asia corp bonds: JACI Investment Grade TRI, US govt bonds: Bloomberg US Treasury TR, US corp bonds: Bloomberg US Corporate TR, Euro bonds: Bloomberg EuroAgg TRI, Emerging market bonds: Bloomberg EM USD Aggregate TRI

Safe‑haven flows have been a key driver of this resilience, as global investors increasingly favour Singapore’s strong currency and high‑quality bond market during periods of stress. This demand has helped Singapore bonds hold up better than global peers, especially during bouts of volatility.

With markets anticipating MAS to tighten policy, the SGD is poised to appreciate further, potentially attracting increased demand for SGD assets such as Singapore government bonds and high‑grade corporate bonds. For foreign investors, a stronger SGD also adds a currency gain to total returns, further enhancing the appeal of SGD bonds and reinforcing price stability.

2. Structural stability keeps yields orderly

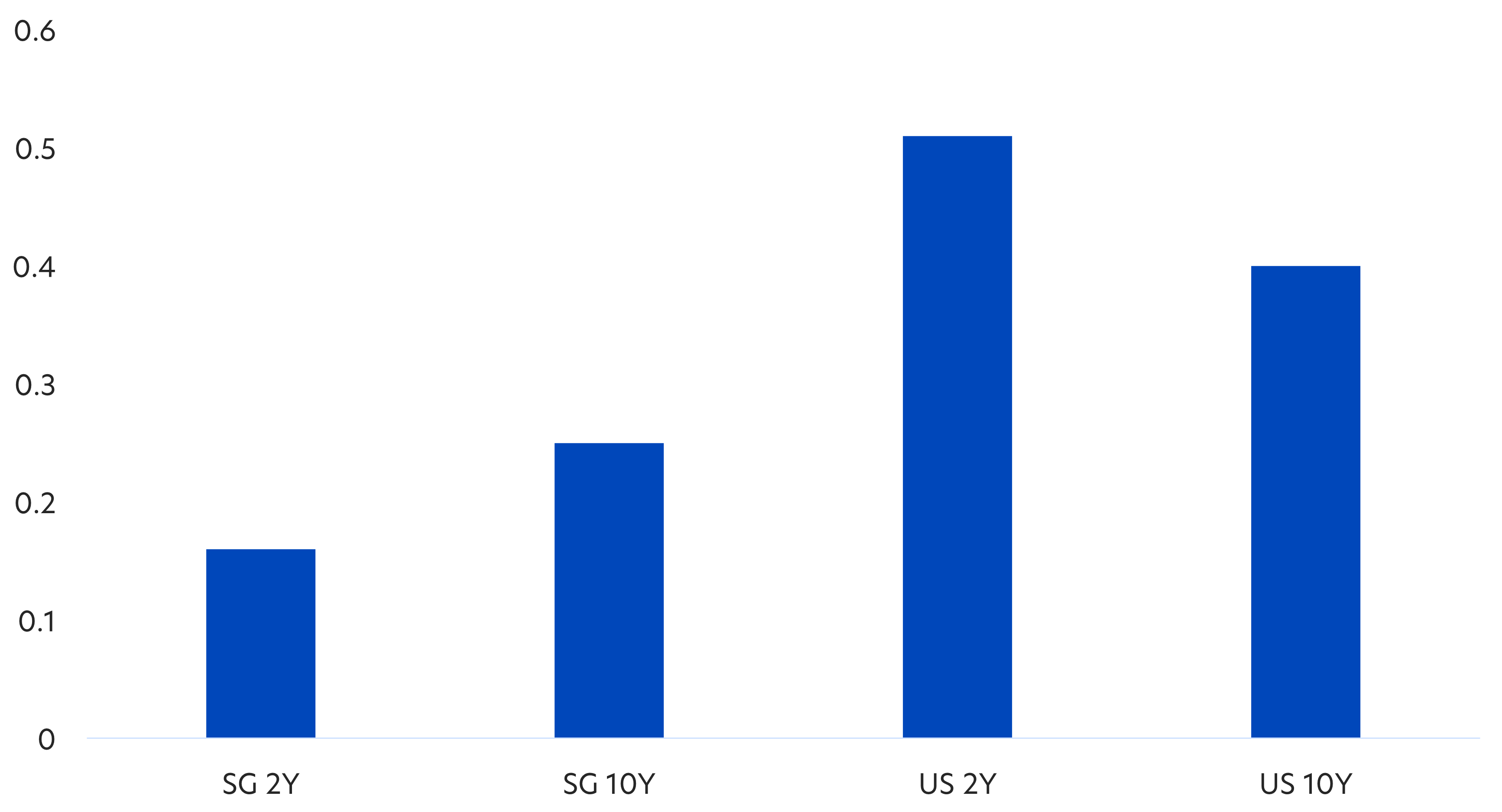

Singapore’s exchange‑rate‑based monetary policy provides another source of stability. By using the SGD NEER to manage inflation rather than relying on sharp interest rate hikes, MAS delivers a more predictable inflation path and a more stable rates environment than many regional or developed markets. This helps to dampen yield volatility and support bond price stability.

These dynamics are visible today. Despite a sharp rise in US Treasury yields following higher global energy prices, Singapore government bond yields have moved only modestly higher, reflecting their relatively low correlation with US Treasuries and Singapore’s strong policy credibility. For example, the yield on Singapore’s 2‑year government bond has risen by just 0.16 percent, compared with a 0.51 percent increase in the US 2‑year Treasury.

As a result, Singapore government bonds have outperformed US Treasuries in recent months, underscoring their safe-haven appeal amid geopolitical and inflation uncertainty.

Fig 2: Increase in Singapore government bond yields vs US Treasury yields (%) (27 Feb – 25 Mar 2026)

Source: Bloomberg, as of 25 Mar 2026. Note: Higher yields correspond to lower bond prices.

3. Strong fundamentals underpin credit resilience

The supportive macro backdrop extends to corporate credit. High‑grade SGD corporate bonds, issued largely by statutory boards, financial institutions, and Temasek‑linked companies, have remained notably resilient, with spreads widening far less than global credit indices during the Iran‑related volatility. This reflects not only strong issuer fundamentals but also the stability of the SGD rates environment and steady local institutional demand.

Singapore’s broader economic resilience further reinforces credit quality. With industrial production, PMI readings and non‑oil domestic exports holding firm, and GDP growth forecast at 2 to 4 percent for 2026, Singapore remains one of the region’s more resilient economies. This reduces downgrade risk and keeps default probabilities among the lowest in Asia, factors that help anchor corporate bond valuations even as global credit markets experience bouts of stress.

Takeaway

In sum, with the prospect of a stronger Singapore dollar and continued safe‑haven flows into SGD assets, Singapore bonds are entering a more favourable phase. They offer investors a compelling blend of stability and relative outperformance in an otherwise uncertain global environment.

| If you are interested in investment opportunities related to the theme covered in this article, here are some UOB Asset Management Funds to consider: United SGD Fund

United Singapore Bond Fund

|

This document is for general information only. It does not constitute an offer or solicitation to deal in units in the Fund (“Units”) or investment advice or recommendation and was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. The information is based on certain assumptions, information, and conditions available as at the date of this document and may be subject to change at any time without notice. No representation or promise as to the performance of the Fund or the return on your investment is made. Past performance of the Fund or UOB Asset Management Ltd (“UOBAM”) and any past performance, prediction, projection or forecast of the economic trends or securities market are not necessarily indicative of the future or likely performance of the Fund or UOBAM. The value of Units and the income from them, if any, may fall as well as rise, and is likely to have high volatility due to the investment policies and/or portfolio management techniques employed by the Fund. Investments in Units involve risks, including the possible loss of the principal amount invested, and are not obligations of, deposits in, or guaranteed or insured by United Overseas Bank Limited (“UOB”), UOBAM, or any of their subsidiary, associate, or affiliate (“UOB Group”) or distributors of the Fund. The Fund may use or invest in financial derivative instruments, and you should be aware of the risks associated with investments in financial derivative instruments which are described in the Fund’s prospectus. The UOB Group may have interests in the Units and may also perform or seek to perform brokering and other investment or securities-related services for the Fund. Investors should read the Fund’s prospectus, which is available and may be obtained from UOBAM or any of its appointed agents or distributors, before investing. You may wish to seek advice from a financial adviser before making a commitment to invest in any Units, and in the event that you choose not to do so, you should consider carefully whether the Fund is suitable for you. Applications for Units must be made on the application forms accompanying the Fund’s prospectus.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

UOB Asset Management Ltd Co. Reg. No. 198600120Z