3. Investment model

The Digital Adviser’s investment model is designed with the following key unique features:

Forecasting

Unusual event shocks are taken into consideration that typical mean-variance optimisation models may not. This enables a more realistic analysis of downside risk in the forecasting model and a more accurate estimate of the success

probability.

Customising solutions based on an investor’s investment horizon

The model utilises an algorithm to scale risk levels according to the time horizon of an investor, as capacity to take risk and the probability to achieve a goal is inversely related to the duration of the investment horizon. Embedded in

the model is an overlay function that “glides down” the risky assets allocations, known as the “glide-path”, which automatically adjusts the portfolio rebalancing (see para 4.5) based on an investor’s remaining investment horizon.

These features enables the Digital Adviser to cater dynamically for complex or future contribution strategies, multiple savings and spending goals to closely reflect real life financial planning.

Glide-path solution

The Digital Adviser targets to maximise returns for your specified risk level based on your risk profile and investment horizon.

We adopt a risk-based approach where your volatility tolerance level is a key factor in determining the recommended portfolio.

In addition, your investment horizon is taken into consideration, where we gradually adjust the portfolio-solution risk by systematically switching from assets with higher risk to more conservative ones as we draw closer to the end of

your target investment horizon.

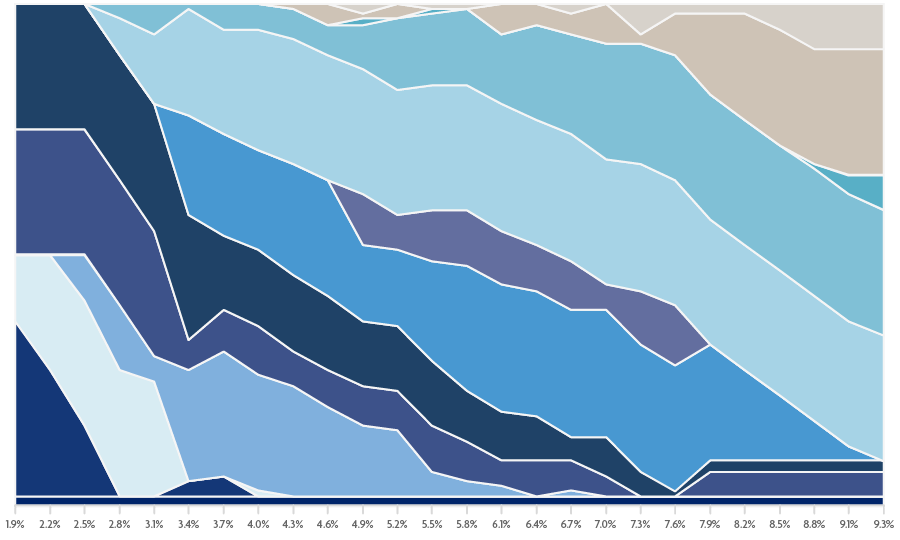

Asset allocation by volatility target

Figure 1

-

Money Market or Equivalents (Singapore)

-

Government Bonds (Singapore)

-

Government Bonds (US)

-

Investment Grade (Asia)

-

Investment Grade (Global)

-

High Yield (Asia)

-

High Yield (Global)

-

US Equity

-

Asia Ex-Japan Equity

-

Singapore Equity

-

Europe Equity

-

Global Equity

-

Cash Balance

Figure 1 presents a chart of the asset class weight as a function of the portfolio (solution) volatility. The non-linear shape of these allocations or weights is caused by the weighting constraints and non-linear

nature of the glide-path.

Figure 1 is for illustration purposes only as configuration parameters and inputs can change.

Asset class selection

In Digital Adviser, asset class selection is based on two main objectives – to align with the goals of corporate investors and to ensure diversification of risk. Only liquid assets are included to enable corporate investors with the

flexibility to invest based on their investment goals and horizons.

With the efficient frontier, we aim to balance and limit the number of asset classes3 to a reasonable level and also deploy a forward-looking optimisation model.

For each asset class, UOBAM IM-MA will identify and recommend the most appropriate mutual funds or ETFs to gain exposure to the specific asset classes. Currently, our universe of instruments is confined to UOBAM funds and ETFs listed

on NYSE and NASDAQ. Our methodology compares UOBAM funds and passive index trackers. Selected UOBAM funds would constitute actively managed strategies that have consistent excess returns against their benchmark and better return

performance relative to the amount of risk taken over the passive indices.

Asset classes included are:

Money Market Instruments

Government Bonds

Investment Grade

Corporate Bonds

High Yield Bonds

and Equities

The following selection and screening criteria are being applied:

If a (currency) hedged solution is available, we will select the same currency solution to minimise foreign exchange related risk

Where an investment instrument delivers consistent excess returns against its benchmark and exhibits favourable risk-adjusted returns, we will place weightage on the instrument. (i.e. UOBAM funds or ETFs)

We evaluate performance on the basis of rolling the 3-year and 5-year performances for each investment instrument.

Recommendations to include a UOBAM Fund or ETF on the platform are based on performance analysis with preference given to the instrument with higher consistent excess returns against its benchmark and favourable

risk-adjusted returns.

Capital market assumption inputs

Capital Market Assumptions (CMA) are provided by UOBAM IM-MA. Model inputs cover the asset classes in Digital Adviser, in the respective currency of the proposed advisory solution and reviewed on a quarterly basis.

Key inputs for each asset class include:

Expected return forecasts

Volatility estimates

Matrix

of asset class correlation assumptions

Recommendations to include a UOBAM Fund or ETF on the platform are based on performance analysis with preference given to the instrument with higher consistent excess returns against its benchmark and favourable risk-adjusted returns.In

addition to the market equilibrium implied returns, we also use data on historical returns, interest rates, credit spreads, forward-looking return expectations, earnings growth, and other macroeconomic variables to form long-term expected

return views for each asset class.

We use a two-tier CMA implementation approach: mid-term and long-term forecasting processes. We design and provide a blended solution for input onto the Digital Adviser’s optimiser. These CMA are expressed through expected returns,

volatility of returns for each asset class, and their correlations.

Return estimation

Equities asset classes

Return forecasts are derived by combining two forward-looking estimation models, one based on forward-earnings and the other based on earnings smoothened for extreme outcomes.

Fixed Income asset classes

Money market asset class:

Returns are derived based on UOBAM’s medium-term forecasts for inflation and Inter-Bank rates.

Government Securities Index:

Returns are estimated based on medium-term forecasts when it comes to assumptions of inflation, interest rates and yield curve movements. Return estimates incorporate resulting

capital gain-loss factors and are annualised.

Investment Grade Credit and High Yield Credit Index:

Returns are estimated by adding a risk-adjusted credit spread to the relevant Government Security curve to derive return estimations.

Risk estimation

Risk (volatility) estimation is based on the average 5-year and 10-year rolling volatility of returns. We define both the 5-year and 10-year volatility as the geometric average to smooth the result.

Correlation estimation

Matrix of correlation assumptions are based on 5-year rolling returns with adjustments based on UOBAM’s investment views so that we can forecast with longer persistency and higher stability of estimation.

Optimisation Model

Our optimisation model is a forward-looking financial model, providing probabilistic outcomes about the future portfolio performance or a list of projections to suit your investment plan or risk profile.

We focus on managing the risk level, evaluate, and monitor potential loss metrics, similar to Value at Risk or even Conditional Value at Risk.

Separately at each asset class level, we replicate different market behaviour principles especially when it comes to idiosyncratic characteristics and/or historical periods for these respective asset classes. The model incorporates

market shocks or “jumps” on top of a financial modelling process that auto-regresses around average values given by market assumptions. This enables portfolios to have better sensitivity as compared to models focused on historical

observations, which are based on normally distributed events.

Our optimisation model is closer to a “real-world” financial model, and is designed to consider and implement the multiple-goal planning process, with visibility on the probability of achieving your goals.

Setting limits and constraints

We aim to limit the degree of shift in allocations, to achieve greater stability and better alignment with investors’ risk tolerance and investment objectives.

The applied optimisation model aims to avoid scenarios like:

-

Significant change in allocation when there are modest changes in the model inputs.

-

Irrational allocations as a result of aiming for an optimal Sharpe ratio4 where risky assets get allocated into very conservative or conservative portfolios.

In addition, there are constraints being implemented on the model to limit allocations and exposures especially when asset classes are relatively highly correlated.

Rebalancing

On a quarterly basis, UOBAM IM-MA reviews our CMA and asset allocations. UOBAM Invest will notify you via email when there is a rebalancing action to re-align the asset allocation of your Digital Adviser portfolio.

After rebalancing is completed, you can continue to track the performance of your investment portfolio against your savings or financial goals and objectives. You can review your contribution or withdrawal plans to improve the

probability of success of achieving your financial goals.